Selling a property is a very complex transaction, especially if you are selling your home. From setting the right price, to advertise the property, presenting it to potential buyers, and finally closing the deal, this process is very time-consuming, and it can cost you a lot of money. This is where a good realtor comes in handy, as they take care of most of the work, without requiring any assistance from your part. Moreover, a good realtor can actually get you a much better deal than you had ever hoped for. So, if you are still not convinced that the 3% commission is worth it, keep on reading to learn the main benefits of working with a realtor when selling a home.

List at the right price :

When you sell your home on your own, your only option is to compare other similar properties that are currently on sale and estimate how much your own property is worth. There are also online tools that you can use to estimate your property, but most of them are very inaccurate. On the other hand, a good realtor with local experience will tell you from the start how much your property is worth. Sure, you can ask for more than what they advise, but even in this scenario, the realtor can help by telling you approximately how long it will take to find a buyer willing to pay the demanded price, or whether or not you have any chances of selling at all.

Marketing expertise :

A good marketing plan should include more than just some online adds. Realtors will expose your property to the general public, but also to other agents through multiple listing services. This means that there will be other agents that could bring in potential buyers. If you don’t want your property to advertise the property, a good realtor will have valuable contacts that can make the deal happen as privately as possible. For example, say you wanted to sell an expensive property in the West Hollywood Real Estate market. You would have to work with a reputable dealer, whose network includes celebrities and wealthy investors. Moreover, a good realtor can also provide you with better home presentations. Since most of them also work with buyers, they know what small presentation details usually make a positive impact on potential buyers.

Security :

When selling a home on your own, you need to take a lot of precautions to ensure your safety. Bringing strangers into your home can be very dangerous, especially when it comes to private presentations. Keep in mind that not everybody will have the availability to attend open house events, so you will often have to bring potential buyers at home in the evening or early in the morning. However, if you work with a realtor, you don’t have to worry about these problems, as they will take care of screening the candidates, and they will handle all the presentations on their own.

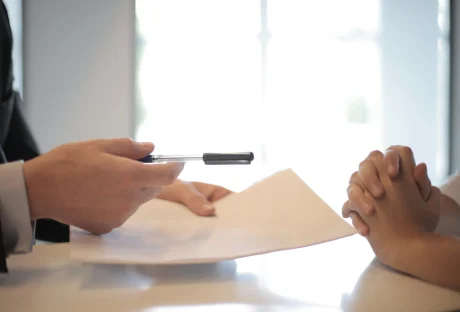

Negotiating and closing experience :

First of all, the negotiation process is very tough, and inexperienced sellers can often be fooled into lowering their price on account of small damages. An experienced agent, on the other hand, will stand their ground, and they will know how to highlight a property’s advantages, in order to balance its disadvantages. Moreover, they will also take care of all the paperwork, including the written offers and counteroffers. If potential buyers ask for repairs, the realtor can tell you whether or not it is convenient for you to satisfy their demands. As a seller, your judgment will be clouded by subjective reasons, but you can count on your agent to be objective and protect your interests at all times.

Expert advice :

Whether or not you are a first-time seller, this type of transaction is a significant financial decision, so it pays to have an expert on your side to guide you through this process. There are countless details that can cost you money when dealing with the process of selling a property. You might save a little money if you handle it on your own, but you will increase the risk of encountering problems that could cause you to waste a lot more money than the realtor’s commission.

Read Also :