Published on: 02 February 2021

Last Updated on: 11 September 2024

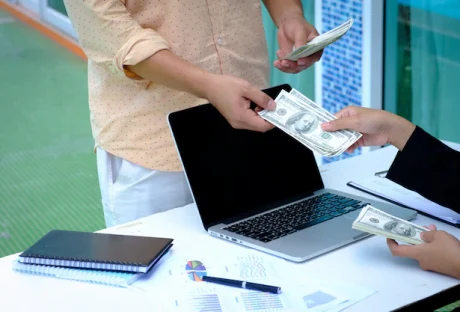

As a small business, you’ll want to make it your priority to begin creating revenue immediately when starting up. This can be difficult, but it will set your company in good stead for what the future brings. Ultimately, you cannot rely on funding.Plus, whatever you have in your pocket to get to where you not only want to be but also need to be. If you’re a small start-up, continue reading to find out four ways you can improve your Startup Revenue.

Try to Have Immediate Cash Flow

Whilst it is useful having funding to create and attempt to grow your start-up, this money can be over rather quickly. Especially when you work out what you intend to do with it.That said, it is impossible to continue as a small business without attracting immediate cash flow into the company.Pumping money into the business earlier on will provide you with a great immediate start-up. However, it is essential that you make sure this money is spent on the right things and not useless items. It is possible to invest, too, but your investments are not wholly reliable.Therefore, experts recommend that you attempt to sell and provide your goods and services. This is from the get-go to have some form of cash flow arriving promptly.

Have Business Insurance

Another practice that will improve your revenue as a small business start-up is investing in business insurance. For some sectors, it is a legal requirement to have business insurance. Even experts generally recommend that business owners invest in it anyway.Your certificate of insurance It is a great form of protection for your business and employees. This insurance could improve your startup revenue as it could take care of your business. It could also act as a safety net if something was to go wrong.For example, if your premises were broken into two weeks into the operation, the insurance would provide financial compensation.

Recruit within Your Means

Recruiting and hiring staff as a small business can be a daunting task, especially if it’s the first time you’ve tried it. It is important that you don’t attempt to run the entire business yourself. This is because you’ll soon realize that your products and services suffer as a result.Hiring and retaining staff within your means is a reasonable way to improve startup revenue.

Use Social Media

The growth of social media has been an excellent tool for all businesses. It has even been a lifeline for smaller businesses.This is because these businesses essentially don’t have the funding to invest in digital marketing. Therefore, we need to rely on free forms of advertising. Social media being the greatest of all!As a start-up, you’ll save money by marketing yourself, and you’ll also increase revenue by connecting with a large audience online. This way, you’ll gain rapport with customers and clients as well as make money.Consider these tips to improve your startup revenue from the get-go.

How to Improve your Cash Flow as A Startup

Starting a business is all good, but if you don’t have cash flow — a steady flow of incoming cash — your business will go belly up.No matter how great the business idea or product is.

Just Start Selling!

It will never be the perfect time to finally launch that product or service and begin selling!You will have to just bite it and do it for once!You won't be able to start generating revenues if you just keep thinking about how to bring the money!The key to immediate cash flow is to start selling your products or services as soon as possible. You don’t have to wait until everything’s perfect before you begin making sales.Whether it’s pre-orders, minimum viable products, or service contracts, find a way to get money coming in right away.Not only will this help you generate revenue faster, but it will also validate your business concept with real paying customers.

Watch Your Expenses

Every dollar a startup spends should be spent in expectation of ROI. Spend to grow and spend as late as possible, never earlier.Don’t spend money on anything that doesn’t have a direct impact on your growth – especially when you are just starting.

Keep a Close Eye on Your Financials

Review your cash flow statement regularly so you know who is paying you and where your money is going.Then, use that information to help you make better decisions about your spending, pricing, and growth strategy.Not keeping an eye on this will cause unexpected shortages of cash flow but, more importantly, can put you in a financial bind.

To Wrap it Up!

To be a successful startup entrepreneur, you must constantly improve your cash flow.This means selling as early as possible, possibly before you are ready, managing your expenses against sales, offering the right payment terms to customers, and paying close attention to accounts receivable.Read Also:

Content Rally wrapped around an online publication where you can publish your own intellectuals. It is a publishing platform designed to make great stories by content creators. This is your era, your place to be online. So come forward share your views, thoughts and ideas via Content Rally.

After the surge of the pandemic, there has been an increased use of the internet to commence business. This is because it allows people to trade easily and bring about a series of buying and selling stocks and bonds. Also, with the rise of internet users in the world, especially with the rise of smartphones, trading has become easy.

Therefore, in the next section, we will discuss the crucial benefits of online trading. This will allow you to earn a lot and build a future after buying stock as per your investing strategy. Conversely, you can educate yourself on different investment options and ways to earn higher income from the market.

That is why, from youth to old ones, everyone today is interested in the stock market and how it behaves accordingly. This eventually helps everyone to invest their money safely. You can also learn about xauusd hoy from the Roboforex website.

So, kindly look down to begin the discussion.

Benefits Of Online Trading

As discussed earlier, there is a growing trend of using online platforms to trade. In simpler terms, purchase and sell stocks and bonds. This is because you can get better returns from stocks rather than the interest rates of banks.

Leaving aside, here are a few benefits of online trading -

Educate Yourself

One of the biggest benefits of online trading is that with online trading, you can learn a lot about stocks and bonds. This will help you enhance your knowledge of different investment strategies. Eventually, it will help you to earn bigger profits from the market.

Moreover, you can learn about trends and analyze market behavior to spend money better. Hence, with the help of online trading, the modern youth can gain interest in trading and focus on a better future. So, educate yourself with different patterns and enhance your trading skills.

Monitor Your Investments

Another benefit lies in the fact that you can monitor your investments on the online platform. This allows you to know what you have bought and sold on the market. Also, you can see how your stocks are performing throughout the day. Consequently, within the comforts of your home, you can predict the market behavior and spend accordingly.

In other ways, you can invest in stocks and bonds by casually sitting in your room or when you are in your gym. In addition, you can track them from any digital device and follow them properly.

Decentralizes The Trading Process

When it comes to online trading, no premium holder controls the market. In other words, there is no middleman in the process of buying and selling. This means you will have access to all stocks that are available on the stock exchange.

There is no little broker communication who will guide you to stocks and bonds and help you to purchase and sell them. Consequently, this means you can spend less money on the broker fees. Conversely, you can spend that money on the purchase of stocks and bonds. Hence, online trading platforms give more benefits and help to enhance your purchase resume.

Fast Track Your Transaction Process

Another feather in the flock will be the ability to fast-track your transaction process. This way, you can buy and sell stocks in a much easier way. Imagine you saw a bond or stock. You don’t have to go to the broker to buy and sell the stocks and bonds. You can simply select the stock and purchase it.

Hence, you don’t have to worry about going to the New York Stock Exchange to sell stocks. With just one click, you can easily see your stocks. Consequently, it saves you valuable time and energy and helps you earn more profit.

Online Trade Is The Future

In the end, we can agree that online trade is the future. This is because it will bring forth more audiences to trading platforms and allow them to buy and sell stocks. Also, with online trading, you can fast-track your transaction process, which will help you to buy and sell stocks. Hence, you can plan your investing strategy in a better way.

Read Also:

Why Entrepreneurs Should Pay Attention To Cryptocurrencies In 2021

The Profit Revolution: The Best Bitcoin Trading And Investing Platform

Exciting Facts About Cryptocurrency And Crypto Wallets

Investors and developers believe in the prospects of NFT.

Venture capital and crypto funds became interested in the sector in early 2018. So, the company Dapper Labs (developer of CryptoKitties) in 2017 first raised $12 million in funding, in 2018 another $15 million, and in 2019 another $11.2 million.

Game studios Rare Bits and Lucid Sight raised $6 million each, and Immutable (developer of Gods Unchained) received $15 million in funding in September 2019, Mythical Games — $19 million, and the OpenSea marketplace — $2 million.

It is difficult to calculate the exact volume of the NFT market. Non-exchangeable tokens are not traded on conventional crypto exchanges — instead, they are bought or sold mainly for ETH on specialized platforms, fan sites, or inside computer games. The largest NFT platforms: Opensea, Nifty Gateway, Knownorigin, Makersplace, Super rare.

According to the NonFungible website, the total sales of the ten most popular NFT projects amounted to more than $109.5 million, of which more than $1.8 million was received only in the last 7 days. As you can see, the NTF market is still quite small. But more importantly, its volume is steadily growing. NFT games are brilliantly ruling over the gaming world. You can find some of the best NFT games on this site including lightnite, illuvium, my defi pet, and lost relics

According to the calculations of the publication Decrypt, the volume of trading in the NFT market for the summer of 2020 increased by 57%, which led to an increase in the value of the industry to about $100 million.

According to Dune Analytics, monthly sales in the NFT sector exceeded $ 1-3 million in the summer alone, reaching a peak of $6 million in September of this year. However, according to the art platform SuperRare, only in October they sold digital works worth more than $4.34 million.

Lot's of numbers here. To learn about NFTs, follow the FAQ NFTs: Everything You Need to Know About NFTs.

NFT can Create a billion-dollar Market and Popularize Blockchain:

NFT is a promising sector for the development of the crypto market with hundreds of millions of potential users: sports, pop culture, computer games, and art lovers who are willing to pay for their hobbies.

Therefore, startups that bet on this direction have something to compete for. Most likely, it is for these markets that we will soon see sharp competition.

But it is not worth waiting for the triumphant boom of the market of non-interchangeable tokens. Such tokens have long been known to the players of the crypto market, but have not yet received a truly mass application. So far, the belief in NFTs among their developers and investors is stronger than the need for them among crypto users.

So, for example, to become popular among hundreds of millions of gamers, gaming cryptopredmetry in the NFT format must be integrated into the most popular video games. But it is not profitable for their developers, because they can lose a significant part of their income.

Sports and music fans, art aficionados and collectors are also only looking at NFT for now. Those, although they belong to only one owner, do not allow you to interact with the underlying asset physically — and without this, the same digital picture is not much different from the reproduction.

Another difficulty is technical. Tokens on Ethereum are too dependent on their network, which is not yet suitable for mass use. That is why the same CryptoKitties game switched to the new Flow blockchain in May 2020. However, after the beginning of the upgrade of Ethereum to the 2.0 state, the scaling problem should gradually disappear.

Will the NFT be used outside of digital art? Hard to answer. 2mcuchfoffee also researched the topic and come up with the paper.

In any case, it is great that NFT startups understand all the difficulties and do not give up trying to create a new market, explore ways to use the technology, and monetize it. If the enthusiastic expectations about this market come true, his works will hit the jackpot.

But to do this, it is necessary to conduct "explanatory work" and clearly prove to a wide audience the advantages of NFT.

Read Also:

Everything You Must Know About Bitcoin Circuit: Legal or Scam

Exciting Facts About Cryptocurrency And Crypto Wallets

Best Crypto Trading Bots of 2020: You are Unaware

In a fast-paced world where financial emergencies can arise unexpectedly, many individuals consider payday loans. The advent of the internet has simplified the process, allowing potential borrowers to apply for payday loans online. Here, kicks the need for direct lenders.

However, navigating this terrain requires caution to ensure both the safety and the appropriateness of the financial solution. This article aims to guide you through the process of applying for direct lender online loans in a safe and informed manner.

Understanding Payday Loans

Before diving into the application process, it's crucial to understand what payday loans are. These loans are typically characterized by their brief duration and relatively high-interest rates, with the repayment usually scheduled for the borrower's upcoming payday.

They frequently serve as a financial solution for unforeseen expenses or a means to manage finances until the next salary is received.

Who Are Direct Lenders?

In the financial ecology, a direct lender is any bank or financial institution that finances and approves mortgage-based loans. With their inclusion, there is no need for a middleman, which eventually speeds up the process. Furthermore, a direct lender is compensated through multiple charges and fees.

They are usually different from a mortgage broker because the latter is a financial expert who brings a lender and a borrower together. Like lenders, they do not utilize their personal funds for advancing mortgage loans.

Choosing Direct Lenders

When it comes to online payday loans, there are two main types of lenders: direct lenders and third-party lenders. Direct lenders manage the loan process from start to finish, while third-party lenders act as intermediaries.

Opting for direct lender online loans offers more transparency and fewer additional fees. Here are some steps to do so:

1. Researching The Lender

The first step in the safe application for a payday loan is thorough research. It's important to verify that the lender is legitimate and reputable. You can do this by checking for online reviews, looking for any filed complaints against the lender, and ensuring they have a valid license to operate in the borrower's state.

2. Understanding The Terms

Before applying, it's vital to understand the terms of the loan fully. This includes the interest rate, fees, repayment terms, and any fines for late or missed payments. Reading the fine print can prevent unpleasant surprises later on.

3. Direct Lenders' Application Process

The process for online payday loans is typically straightforward. Borrowers must be competent enough to provide personal and financial information. For example, proof of income, employment details, and bank account information. Ensuring that the lender's website is secure and uses encryption to protect personal information is key.

4. Assessing Affordability

Before taking out a payday loan, evaluating whether it is affordable is crucial. This means considering if the borrower can repay the loan on time without causing financial strain. It's advisable to look at the budget and weigh if the loan is truly necessary.

Drawbacks Of Hiring Direct Lenders

It is true that direct lending decreases the dependency on a financial entity or bank. But, it comes with its own set of risks and challenges. Given below are a few disadvantages of working with a direct lender. Before you hire someone, make sure to go through these properly, assess the risks, and start working towards them efficiently:

A. The Risks Involved

While payday loans can be a convenient short-term solution, they come with risks. The increasing charges, as well as interest rates, can create a cycle of debt if one does not tackle them with caution. Understanding these risks is fundamental to making an informed decision.

B. Risk Of Application Denial

Another con of working with a direct lender is your application’s approval. They might have their own loan terms and understanding of the same. Hence, if there is any error in your application that doesn’t make sense to them, chances are high that your loan will get denied. As a result, you will come back to the exact same place from where you started- the loan application!

C. Privacy and Security

When applying for payday loans online, protecting personal information is paramount. This means ensuring the lender's website is secure and not providing personal information on public or unsecured networks.

Conclusion

Applying for payday loans online from direct lenders can be a straightforward process, but it requires careful consideration and research. Understanding the terms, assessing affordability, and ensuring the security of personal information are all crucial steps.

While payday loans can provide immediate financial relief, they are not a long-term financial solution and should be used judiciously. Being informed and cautious can help navigate the process safely and responsibly.

Read Also:

Finding the Best Mortgage Lenders to Buy Your Dream House

Why Are Lenders Moving Towards Automated Mortgage Processing?

Private Money Lenders – Here Is Why This Is A Great Alternative For Your New Business

Whilst it is useful having funding to create and attempt to grow your start-up, this money can be over rather quickly. Especially when you work out what you intend to do with it.

That said, it is impossible to continue as a small business without attracting immediate cash flow into the company.

Pumping money into the business earlier on will provide you with a great immediate start-up. However, it is essential that you make sure this money is spent on the right things and not useless items. It is possible to invest, too, but your investments are not wholly reliable.

Therefore, experts recommend that you attempt to sell and provide your goods and services. This is from the get-go to have some form of cash flow arriving promptly.

Whilst it is useful having funding to create and attempt to grow your start-up, this money can be over rather quickly. Especially when you work out what you intend to do with it.

That said, it is impossible to continue as a small business without attracting immediate cash flow into the company.

Pumping money into the business earlier on will provide you with a great immediate start-up. However, it is essential that you make sure this money is spent on the right things and not useless items. It is possible to invest, too, but your investments are not wholly reliable.

Therefore, experts recommend that you attempt to sell and provide your goods and services. This is from the get-go to have some form of cash flow arriving promptly.

Another practice that will improve your revenue as a small business start-up is investing in business insurance. For some sectors, it is a legal requirement to have business insurance.

Even experts generally recommend that business owners invest in it anyway.

Your certificate of insurance It is a great form of protection for your business and employees.

This insurance could improve your startup revenue as it could take care of your business. It could also act as a safety net if something was to go wrong.

For example, if your premises were broken into two weeks into the operation, the insurance would provide financial compensation.

Another practice that will improve your revenue as a small business start-up is investing in business insurance. For some sectors, it is a legal requirement to have business insurance.

Even experts generally recommend that business owners invest in it anyway.

Your certificate of insurance It is a great form of protection for your business and employees.

This insurance could improve your startup revenue as it could take care of your business. It could also act as a safety net if something was to go wrong.

For example, if your premises were broken into two weeks into the operation, the insurance would provide financial compensation.