Published on: 01 April 2023

Last Updated on: 03 April 2023

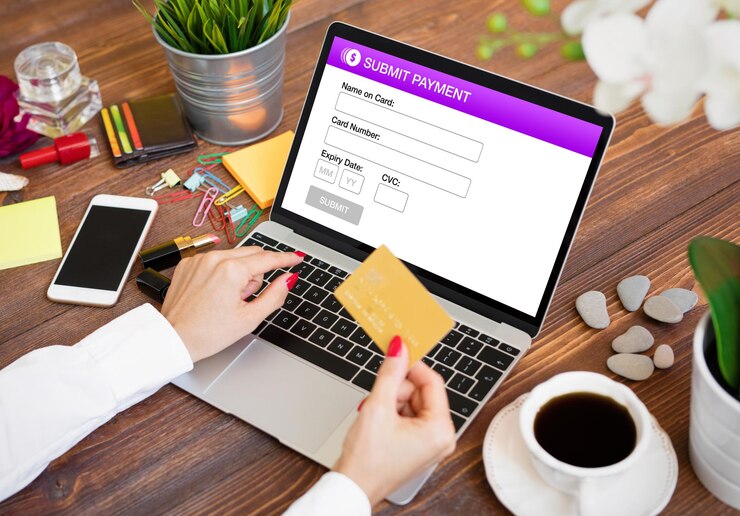

The use of an online event payment solution simplifies the entirety of an event's financial administration as well as the processing of payments. It makes safe transactions easier to complete and is compatible with a variety of payment gateways, including PayPal, credit cards, Authorize.Net, and others. The hassle of manually managing cash may be eliminated with the aid of payment solutions based on the web.

Mistake Payment Administration

Your attendees will have the ability to make payments and donations at any time of day or night thanks to the online payment management system. A system that is PCI-compliant will simplify the process of receiving payments, balancing transactions, managing refunds, addressing chargebacks, and maintaining merchant accounts.

Adaptability In Making Use Of Merchant Accounts

Event planners have the option of utilizing their merchant accounts when they use web-based payment management services instead of managing payments themselves. This account does not cost anything to set up, and it enables you to handle payments made by card as well as those made online. In addition, the payments for the registration are supposed to be sent straight to your bank account with a single click of the mouse.

An Exposition Of The Model Of The Payment Facilitator

The concept of a payfac was developed to facilitate the simplification of the process by which businesses accept electronic payments. Merchants that wished to accept credit card transactions were formerly required to open an account with a merchant acquirer, which may be a bank or a company that was sponsored by a bank.

Is It Possible For Us To Become Into A Payment Processor?

It's not easy, but it's worth it to work toward being a payment facilitator.

The majority of current adopters of the payment facilitator model are software businesses that have built-in payment processing capabilities. For this reason, businesses with established e-commerce, point-of-sale (POS), invoicing, and billing operations are making the switch to empower their client experience, increase their control over that experience, and boost their bottom line.

How To Get Started As A Payment Processor Figure it out

Calculating the potential return on investment is crucial before giving any serious consideration. The payment facilitator model has the potential to increase your software's earnings with each processed transaction, but it will cost you both money and effort to implement.

The value of an undertaking may be gauged via a return on investment study.

Guidelines And Regulations Are Crucial.

Making money off of customers' purchases is only part of being a payment processor. However, when underwriting sub-merchants, there are certain policies and processes that must be followed. The industry and nation in which your sub-merchants operate, their risk tolerance, and the size of your business are all variables you may use as a facilitator to tailor your approach. But, you must establish criteria for at least the following five areas:

Doing Thorough Website Research;

Knowledge of Customers' and Vendors' Data Collection and Analysis. Adjusting to new methods of doing business; Managing transitions in ownership; Doing application reviews manually. Moreover, risk and fraud protection mechanisms must be implemented, and they must work seamlessly within the payment facilitator's verticals.

The Payments Industry's Backbone

If you've gotten this far in your quest to become a payment facilitator, you'll soon reach a crossroads. However, in this crucial stage, you must choose between developing your own infrastructure from the ground up or integrating another party's in order to onboard and serve your sub-merchants.

Putting Pen To Paper On A Sponsorship Deal

Applying to a sponsor, which includes an acquiring bank and a processor, is the next step after establishing the necessary processes and locating the appropriate infrastructure. When that is finalized, a PAYFAC ID (PFID) will be issued to you, allowing you to move forward with underwriting, onboarding, and servicing.

Closing Thoughts

Businesses soon realized that being payment facilitators allowed them to provide a more streamlined onboarding process for their clients, maintain a greater degree of control over the payments experience, and considerably boost the amount of income generated from payments. However, in recent years, this has increased the number of PAYFAC operating in a wide variety of business sectors and market verticals.

Read Also:

Abdul Aziz Mondol is a professional blogger who is having a colossal interest in writing blogs and other jones of calligraphies. In terms of his professional commitments, he loves to share content related to business, finance, technology, and the gaming niche.

Living and driving in Michigan will mean that you need to have Michigan auto insurance because the state requires all drivers to have adequate coverage if they are going to be on the road. Auto insurance will provide you and your family with financial and liability protection necessary in the event of any accidents or if you are a victim of theft.

The cost of insurance in Michigan has been rising the past few years just as the population has. As of 2019, Michigan has a little over 9.987 million people living in the state with a lot of the people in Detroit, Motown, Grand Rapids, Warren, Sterling Heights, Lansing, Ann Arbor, and Flint.

The Tort System:

When you are looking at Michigan auto insurance quotes you may run across information about the tort system which is used in a few states. This means that when an accident occurs someone must be held liable, or guilty for its occurrence. This person and their low-cost auto insurance Michigan are responsible for covering the damage and medical costs for both sides. The person who is guilty will then have the added repercussion of increased premiums.

Minimum Amounts:

Auto Insurance Michigan comes with a few different options. First, you will want to understand what kind of coverage you must have at a minimum, especially if you are considering a no down payment car insurance. The minimum requirement for Michigan state auto insurance is 50/100/25-this means 50,000 for any injuries to a person and 100,000 when more than one person is involved and coverage as the minimum limit for damage of 25,000 as the most basic requirements.

You should also check out sr22 insurance michigan if you're a high risk motorist. Because of these requirements, you should make sure to ask plenty of questions when getting auto insurance quotes in Michigan.

Getting Cheap Auto Insurance in Michigan:

Don't go with a no-name auto insurance company located in the middle of nowhere in Michigan. Go with trusted licensed MI insurance companies whom you can feel comfortable and secure that they will be able to go to should you get into any accidents. Shop around among different Michigan auto insurance companies to get the cheapest rate possible. More competition between the different auto insurance companies in MI means better savings for you, the consumer.

Remember to compare the entire policy and not just the price. Some car insurance companies may offer low rates but may not cover any more than what is required by law.

Another way to get cheap car insurance with no down payment in Michigan is to maintain a good driving history with no speeding tickets or accidents.

Other Ways to Lower Car Insurance Costs-

1. Auto Insurance Discounts:

Take advantage of special discounts available to those who insure their home and automobile with the same Michigan insurance company.

Other Common Ways to Get Discounts:

Be a good student

Get Car Safety Equipment Like Air Bags

Install anti-theft devices

2. Increase your Deductible:

Increase your deductible to the highest amount you can afford. The keyword is affording. The deductible is the amount you need to pay out of your own pocket before the auto insurance company starts to pay for anything. The higher amount your insurance deductible is, the lower your rate will be. Do not increase your deductible to $1,000 from $500 if you do not feel comfortable paying $1,000 out of pocket.

3. Insuring Home and Auto:

By insuring your vehicle and home with the same company, consumers can save as much as 20% on their total premiums between the two policies. Insure MI's free online form allows you to apply for a quote for the home and auto insurance combo to see how much your insurance policy will cost.

Insurance Fraud in Michigan:

There was a recent report that Michigan is the number one state in the US for cheap Michigan auto insurance that is a fraud. In fact, in 100,000 residents there were more than 150 cases of fraud. What this means for you is that when you are searching for cheap auto insurance with no down payment you really need to keep your focus on the traditional providers. If you end up driving under fraudulent insurance you can wind up with a ticket, your car impounded, and heavy fines.

Michigan does have a coalition working to eliminate this criminal offense. They work together with the different law enforcement departments to break up different rings. One raid, in particular, helped save more than 15 million dollars, which also helped to reduce their rates by close to 25%.

While getting the best auto insurance in Michigan may seem like you should hunt for the least expensive of the possible insurance quotes. Because of the minimum requirements and the high rate of fraud you should certainly consider taking your time, reading through the literature your company provides, and definitely going with a well-known company.

Compare Free Michigan Auto Insurance Quotes Online:

There are many insurance agents in Michigan who can provide you with top-notch quality customer service. Get cheap auto insurance rates in Michigan by comparing free online quotes from MI auto insurance companies in our network including reputable providers like Youngamericainsurance.net, Good2go Auto Insurance, or Rodneydyoung.net. Take advantage of many insurance websites’ free comparison service that allows you to fill out one form and receive offers from multiple competing insurance agents serving everywhere in Michigan such as Livonia, Dearborn, and Battle Creek.

Apply for a free no-obligation quote online and talked to insurance agents to see which policies may be best for your situation.

Read Also:

5 Tips For Transport & Logistics Business Owners Before Investing In Insurance

Appliance Repair Process Getting Your Appliances Back In Top Shape

Navigating The Long Haul: Maintaining Your RV’s Black Tank

When you think about life insurance, you think about the financial security it will provide your family when you die. What most people don’t know is that life insurances do not cover every type of death.

Term life insurance is the most common and affordable type of life insurance policy. Term life insurances specific number of years before the policy expires.

You then have the option of renewing it. If you die during the term, however, your insurance will provide death benefits to your beneficiary.

You should know that life insurance policies have some coverage exceptions. Particularly when it comes to the type of death.

This is an important consideration as you purchase a life insurance policy, or if you are continuing to manage one.

Deaths Not Covered by Term Life Insurance

There are certain reasons why your term life insurance won’t payout upon your death.

These coverage exceptions can be a hassle for beneficiaries and loved ones. Especially those who rely on your life insurance to cover medical, funeral, or burial expenses. Deaths which might not have coverage through insurance.

Fraudulent Deaths

If you commit life insurance fraud or someone lies about the cause of death, your life insurance company may refuse to pay death benefits.

It is important, to be honest, and forthcoming when applying for life insurance. Especially if you have any medical conditions or dangerous conditions you are in.

Dangerous Hobby-Related Deaths

If your lifestyle is dangerous or you have dangerous hobbies, these activities may affect your life insurance. For example, certain pilots must opt-in for special aviation coverage to get life insurance.

If someone dies in a flying accident, beneficiaries will not get death benefits.

If you regularly engage in dangerous hobbies like– bungee jumping, scuba diving, or free-climbing – you need to inform your insurance agent or carrier upfront. You may need to list these hobbies or opt for additional coverage.

You may also have a higher premium. Be honest, even if it does mean a higher premium. As noted previously, if you lie on your application or about the cause of death, your beneficiaries are the ones who will suffer.

Murder

If one of your beneficiaries murders you with the intent of collecting your insurance money, they won’t prevail.

The Slayer statute prohibits death benefits from being paid out to anyone who murders or is tied to the murder of the insured. If this happens, death benefits will be distributed to your contingent beneficiaries or your estate.

Suicide

Most life insurance policies have a “suicide clause”. This clause states that if you commit suicide during the first two years the policy is active, then the policy will not cover the death or pay death benefits.

This is designed to prevent individuals from obtaining a policy and then immediately committing suicide.

If the death is possibly suicide, such as a drug overdose, then the insurance company may deny coverage.

They will have to prove that the insured committed suicide (the death was deliberate) and not the result of an accident.

Make Sure You Understand Your Life Insurance Policy

As you can see, there are a variety of situations that could result in your life insurance refusing to pay death benefits to your loved ones.

You should talk to you insurance agent to find out specifically what is and is not covered by your term life insurance policy.

Make sure your insurance agent is up to date on any medical conditions you have or any changes in your hobbies or occupation.

Doing so can help prevent your loved ones from experiencing the unfortunate scenario that is a life insurance coverage denial.

Common Misunderstandings About Life Insurance Exclusions

It's easy to assume that your loved ones are fully covered once you have a life insurance.

Are they?

But as you’ve seen, not all deaths are covered by term life insurance policies. It’s crucial to understand these exclusions clearly.

There are often misconceptions, like believing every type of accident or unforeseen circumstance will be covered, which isn't always the case. Knowing the details is key to avoiding unpleasant surprises later.

Reviewing Your Life Insurance Regularly

Your life circumstances can change, and so should your life insurance coverage. For instance, you might pick up a new hobby that could impact your coverage.

It is a good habit to regularly review your policy with your insurance agent. This ensures that any updates on your health, hobbies, or job are recorded.

Doing this can also give you peace of mind, knowing that your policy remains relevant to your current situation.

Final Note: Clarity is Key

Understanding what your term life insurance covers—and what it doesn’t—is vital. No one wants their loved ones to face unnecessary hurdles during difficult times.

Take the time to sit down with your insurance agent. Ask questions, review potential exclusions, and make sure everything is transparent.

A few efforts today can make all the difference for your beneficiaries tomorrow!

Read Also:

A Detailed Guide to Cashless Car Insurance Policy

Insurance- Need of the time

How Private Hire Insurance Takes You Out from Problems?

Self-employed Health Insurance: Best Types for Every Freelancer

Trading can be a great way to make money, but it’s also very complex and risky. Whether you’re a novice trader or an experienced investor, understanding the basics of trading is essential for success. Today, this WB Trading review will give you ten tips for trading.

Set Realistic Goals

Before you start investing, set realistic goals for yourself so that you know what kind of returns you should expect from your investments. This will help keep your expectations in check and prevent disappointment if and when things don’t go as planned.

Do your Research

It’s essential to do your research before investing in any asset class or financial product. Read up on the types of investments available and compare their features, risks, rewards, and associated costs to decide which is right for you.

Manage Risk

Risk management is critical when it comes to trading successfully. Ensure you understand the risks associated with each investment before committing any capital to them to minimize losses and maximize gains.

Start Small

When starting, it’s best to start with small trades and build up your knowledge and experience as time goes on. Once you have more experience, consider increasing the size of your transactions or taking on riskier investments such as derivatives or options contracts.

Investigate Fees

Fees can eat into profits quickly, so ensure you always investigate the costs associated with any trade before entering it. This way, they don’t cut into your bottom line too much once factored in after a completed transaction.

Use Technical Analysis

Technical analysis studies financial market price patterns to identify potential profit or capital gains opportunities. This type of analysis involves looking at charts of past market performance to identify patterns that could indicate future price movements, which can tell when to buy or sell an asset for maximum profit potential.

Create a Trading Plan

A well-developed trading plan should include goals, strategies, risk management plans, and entry or exit points for each trade you make to maximize profits while minimizing losses. A good plan should also include specific rules you follow no matter what happens in the market so that you stay disciplined when making your trades.

Make Use of Technology

Technology has made it easier for traders of all levels to access markets. Take advantage of online brokers or apps that allow you to monitor trends and open positions quickly and easily from anywhere at any time—this will give you an edge over other traders who are not as tech-savvy or prepared as you may be.

Seek Professional Advice

If, after studying all available trading resources, you still need help or want professional advice, there's nothing wrong with reaching out. Qualified professionals, such as registered investment advisors or stock brokers who specialize in helping new traders, can help you get started correctly without taking on too much risk early on. They may provide insight into potential opportunities within specific market sectors that could benefit new traders looking for consistent investment returns over time.

Monitor Your Trades Regularly

Last but certainly not least, once you've opened up positions on certain stocks or assets, make sure that you're regularly monitoring them. This way, if something goes wrong, you'll know what's happening and why those changes are occurring so quickly! This will help prevent losses from bad moves while allowing for more informed decisions when it comes time to close positions or open new ones!

Final Thoughts

Trading can be profitable if done right, but it’s also a high-risk activity that requires careful consideration at every step. By following the tips in this WB Trading review, traders of all levels can ensure that they set themselves up for success no matter what market conditions prevail at any given time. With some luck and hard work, anyone can become a successful trader!

Additional:

5 Best New Cryptocurrencies To Buy in 2022

Is there a Place for Bitcoin in the Fashion World?

How Many Types Of Entrepreneurs Are There In 2022?

How To Invest In Cryptocurrency Without Buying Any?

Your attendees will have the ability to make payments and donations at any time of day or night thanks to the online payment management system. A system that is PCI-compliant will simplify the process of receiving payments, balancing transactions, managing refunds, addressing chargebacks, and maintaining merchant accounts.

Your attendees will have the ability to make payments and donations at any time of day or night thanks to the online payment management system. A system that is PCI-compliant will simplify the process of receiving payments, balancing transactions, managing refunds, addressing chargebacks, and maintaining merchant accounts.

If you've gotten this far in your quest to become a payment facilitator, you'll soon reach a crossroads. However, in this crucial stage, you must choose between developing your own infrastructure from the ground up or integrating another party's in order to onboard and serve your sub-merchants.

If you've gotten this far in your quest to become a payment facilitator, you'll soon reach a crossroads. However, in this crucial stage, you must choose between developing your own infrastructure from the ground up or integrating another party's in order to onboard and serve your sub-merchants.