Published on: 01 April 2023

Last Updated on: 03 April 2023

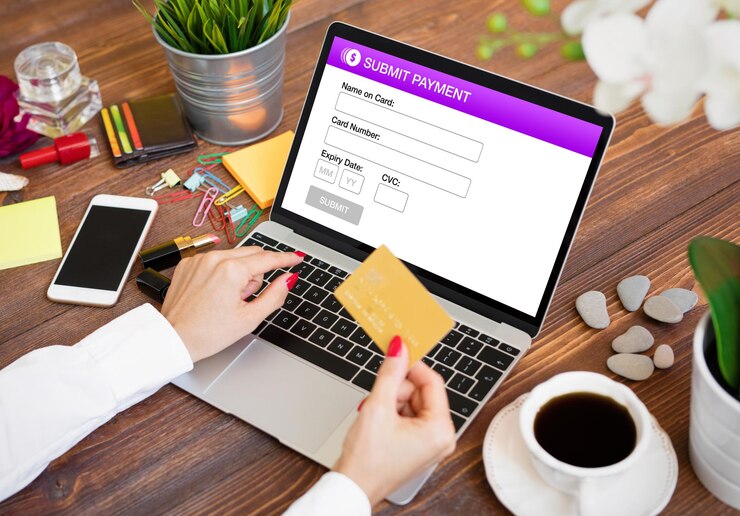

The use of an online event payment solution simplifies the entirety of an event's financial administration as well as the processing of payments. It makes safe transactions easier to complete and is compatible with a variety of payment gateways, including PayPal, credit cards, Authorize.Net, and others. The hassle of manually managing cash may be eliminated with the aid of payment solutions based on the web.

Mistake Payment Administration

Your attendees will have the ability to make payments and donations at any time of day or night thanks to the online payment management system. A system that is PCI-compliant will simplify the process of receiving payments, balancing transactions, managing refunds, addressing chargebacks, and maintaining merchant accounts.

Adaptability In Making Use Of Merchant Accounts

Event planners have the option of utilizing their merchant accounts when they use web-based payment management services instead of managing payments themselves. This account does not cost anything to set up, and it enables you to handle payments made by card as well as those made online. In addition, the payments for the registration are supposed to be sent straight to your bank account with a single click of the mouse.

An Exposition Of The Model Of The Payment Facilitator

The concept of a payfac was developed to facilitate the simplification of the process by which businesses accept electronic payments. Merchants that wished to accept credit card transactions were formerly required to open an account with a merchant acquirer, which may be a bank or a company that was sponsored by a bank.

Is It Possible For Us To Become Into A Payment Processor?

It's not easy, but it's worth it to work toward being a payment facilitator.

The majority of current adopters of the payment facilitator model are software businesses that have built-in payment processing capabilities. For this reason, businesses with established e-commerce, point-of-sale (POS), invoicing, and billing operations are making the switch to empower their client experience, increase their control over that experience, and boost their bottom line.

How To Get Started As A Payment Processor Figure it out

Calculating the potential return on investment is crucial before giving any serious consideration. The payment facilitator model has the potential to increase your software's earnings with each processed transaction, but it will cost you both money and effort to implement.

The value of an undertaking may be gauged via a return on investment study.

Guidelines And Regulations Are Crucial.

Making money off of customers' purchases is only part of being a payment processor. However, when underwriting sub-merchants, there are certain policies and processes that must be followed. The industry and nation in which your sub-merchants operate, their risk tolerance, and the size of your business are all variables you may use as a facilitator to tailor your approach. But, you must establish criteria for at least the following five areas:

Doing Thorough Website Research;

Knowledge of Customers' and Vendors' Data Collection and Analysis. Adjusting to new methods of doing business; Managing transitions in ownership; Doing application reviews manually. Moreover, risk and fraud protection mechanisms must be implemented, and they must work seamlessly within the payment facilitator's verticals.

The Payments Industry's Backbone

If you've gotten this far in your quest to become a payment facilitator, you'll soon reach a crossroads. However, in this crucial stage, you must choose between developing your own infrastructure from the ground up or integrating another party's in order to onboard and serve your sub-merchants.

Putting Pen To Paper On A Sponsorship Deal

Applying to a sponsor, which includes an acquiring bank and a processor, is the next step after establishing the necessary processes and locating the appropriate infrastructure. When that is finalized, a PAYFAC ID (PFID) will be issued to you, allowing you to move forward with underwriting, onboarding, and servicing.

Closing Thoughts

Businesses soon realized that being payment facilitators allowed them to provide a more streamlined onboarding process for their clients, maintain a greater degree of control over the payments experience, and considerably boost the amount of income generated from payments. However, in recent years, this has increased the number of PAYFAC operating in a wide variety of business sectors and market verticals.

Read Also:

Abdul Aziz Mondol is a professional blogger who is having a colossal interest in writing blogs and other jones of calligraphies. In terms of his professional commitments, he loves to share content related to business, finance, technology, and the gaming niche.

Your financial plan should reflect who you are and what matters most to you. By aligning your money management with your core values, you create a more meaningful and fulfilling financial life.

Here's how to make your financial plan match your personal principles:

Identify Your Core Values

As you consider help with financial planning, start by clarifying what's truly important to you. Reflect on what brings you joy and fulfillment.

Consider the causes you care about deeply and how you want to spend your time and energy. Think about the kind of legacy you want to leave.

List your top 5-7 core values. These might include family, health, creativity, learning, adventure, or community. Be specific about what each value means to you.

Assess Your Current Finances

Take stock of your financial situation. Review your income sources, expenses, spending patterns, assets, and debts.

Look at your insurance coverage, investments, and retirement accounts. Identify areas where your money use aligns with or contradicts your values. Look for opportunities to better align your finances with your principles.

Set Value-Driven Financial Goals

Create financial goals that support your core values. If family is a top value, you might aim to build an emergency fund to protect loved ones.

For those who prioritize learning, budgeting for courses or travel that expand your mind could be key. Make your goals specific, measurable, and time-bound. Prioritize them based on your values.

Create A Values-Based Budget

Design a spending plan that reflects your priorities. Allocate more money to areas that align with your values. Cut back on expenses that don't serve your principles.

Leave room for both necessary costs and value-driven choices. This approach ensures your day-to-day financial decisions support what matters most to you.

Invest According To Your Beliefs

Choose investments that match your ethics and goals. This might include socially responsible mutual funds, environmental, social, and governance (ESG) stocks, or community investment options.

Research options thoroughly. Ensure your investment strategy still provides proper diversification and returns.

Plan For Meaningful Experiences

Budget for activities and purchases that truly matter to you. This could include family vacations, skill-building workshops, or tools for a fulfilling hobby.

Prioritize experiences over material goods when they align with your values. This approach often leads to greater long-term satisfaction.

Build A Value-Focused Career

Seek work that resonates with your beliefs and passions. This might mean changing to a more fulfilling job or starting a values-driven side business.

Consider negotiating for a better work-life balance or pursuing additional education for career growth. A career aligned with your values can boost both financial and personal satisfaction.

Give Back Meaningfully

Incorporate charitable giving into your financial plan. Choose causes that deeply matter to you. This could involve regular donations to favorite nonprofits or volunteering your time and skills.

Consider setting up a donor-advised fund or planning for charitable bequests in your estate.

Tips For Successful Financial Planning

Here is how you can begin being a little more responsible with your financial plans.

1. Start Early To Give Yourself More Time

Ever heard the expression, "The best time to plant a tree was 20 years ago, but the second-best time is now"? The same goes for financial planning. The earlier you start, the more your money can grow and compound.

So why wait? Even if you're starting small, it's never too early or too late to set aside some of your income for the future.

Just think, where do you want to be financially in 5 years? How about in 10 years or even 20 years? When you start early, you give yourself some powerful time that can be your best friend when it comes to multiplying your money quickly.

2. Be Realistic

It’s great to have financial goals for yourself, but be sure they are also attainable. If you’re constantly chasing a goal that is impossible to meet, you’ll do nothing more than frustrate yourself in the end.

For instance, if you want to save $50,000 this year on a salary of $40,000 per year and not change your current lifestyle at all, that isn’t going to happen. Instead, set realistic steps for reaching your ultimate goal and celebrate when you hit each one along the way.

3. Seek Professional Advice

Feeling lost? There’s no shame in asking for help. Financial planning can be complicated and confusing, and hiring a professional to assist you is a great way to gain confidence in your plan. Are you investing as much as you could be? Is your tax bill higher than it needs to be?

Can you do more with your resources? A financial planner can address these concerns and many others that might arise, from figuring out how to retire when you want to decide how much life insurance is enough or what steps need to be taken after the death of a loved one.

Having an expert on call is particularly useful when trying to use money as a tool to get the most out of life.

4. Automate Good Habits

Imagine waking up to find your savings account has grown overnight. You haven’t had to do anything. That’s the magic of automation.

By setting up automatic transfers from checking to savings or direct contributions to your retirement or investment accounts, you’ll be building good financial habits without even thinking about it.

And if all your saving and investing goals are on auto-pilot, you won’t need any willpower at all because a single decision will take care of it for you. This is one of the most effective ways I know of to maintain discipline.

5. Educate Yourself

Your best defense to making well-informed decisions is to educate yourself. Are you staying current with financial trends and opportunities that may affect you?

The more knowledge you possess, the better prepared you will be when it comes to taking action with your finances.

It could be learning about socially responsible investments that match your values or how compound interest actually works. Knowledge enables better decision-making on your part and helps alleviate any concerns or fears you may have.

Read articles, attend webinars, or listen to podcasts just like these so that you can continually tweak and improve upon what’s already working.

By aligning your financial plan with your core values, you create a more purposeful and satisfying relationship with money.

This approach leads to better financial decisions and a deeper sense of fulfillment in your financial life. Remember to stay flexible and adjust your plan as life changes occur.

Read Also:

Simplifying Finance: The Role Of UX Design In Financial Services

Alternative Business Financing – What Is It And How Do You Do It?

Embedded Finance In Online Businesses: The Role Of Account Top-Ups And Currency Exchange

In the realm of military service, it's evident that our personnel demonstrate exceptional dedication. Countless individuals are on the frontlines daily, showcasing unwavering commitment and making significant sacrifices for our nation's safety and security. Their courage is consistently acknowledged and appreciated.

However, beneath this commendation lies a less-discussed challenge that many face. A substantial concern, often overshadowed, is the burgeoning issue of medical debts incurred due to their service. This is a pressing matter that merits our attention and understanding.

Understanding The Nature Of Military Service And Health Risks

Within the domain of military service, a spectrum of inherent challenges exists. Daily operations, particularly in high-risk zones, subject our military personnel to many potential hazards. It's worth noting that these risks extend beyond the apparent combat-related injuries. The consistent stress and demands of their roles can manifest in severe long-term mental health complications, PTSD being a notable concern.

As many seasoned veterans have articulated, the repercussions of their service, both visible and latent, often extend far more profound than the casual observer might discern. Such complexities underline the deep nature of military service.

Deciphering Military Health Coverage

TRICARE stands out prominently in the discourse on military health coverage. As our military personnel's primary healthcare program, TRICARE offers a comprehensive suite of benefits. Yet, akin to many insurance packages, it possesses certain complexities. While encompassing an extensive range of medical services, it has coverage gaps.

When juxtaposed with civilian insurance packages, these disparities become markedly evident. For several individuals within the military community, navigating these nuances proves intricate, occasionally culminating in unexpected financial expenditures. This presents a nuanced landscape that warrants closer examination.

Debt Relief Programs: A Beacon Of Hope

There is a beacon of hope in the intricate landscape of medical debt for military personnel and veterans. Active-duty members and veterans can take solace because numerous debt relief initiatives are tailored specifically for them.

These programs, including those focused on veteran debt relief, have garnered significant acclaim, each boasting multiple success narratives. By measures such as reducing the principal debt or formulating structured payment plans, these initiatives serve as instrumental lifelines.

For any military member, veteran, or acquaintance grappling with medical debt, a diligent exploration of these avenues is strongly recommended, offering a pathway to potentially mitigate substantial financial challenges.

By The Numbers: Grasping The Scale Of Medical Debt Among Military Families

Assessing the prevalence of medical debt among military families prompts a deeper inquiry into the available data. This investigation reveals a somewhat concerning scenario. A considerable proportion of military families indeed face the brunt of medical debt. When juxtaposing this reality with civilian families, the disparity becomes conspicuously evident.

Notably, despite the immense sacrifices rendered by military personnel, they frequently encounter more pronounced financial challenges related to health care than many civilians. Such observations underscore the need for a comprehensive examination of the underlying factors.

The Ripple Effect: Beyond Monetary Concerns

Delving into the broader implications of medical debt reveals a multifaceted impact beyond the evident financial strain. Beyond the fiscal ramifications, there is a significant emotional toll. Manifestations include heightened anxiety levels, pervasive stress, and potential feelings of despair.

Additionally, the familial dynamic is not immune to this burden. Once centered on daily life's pleasantries, conversations may shift toward the pressing concerns of impending bills. Future aspirations, such as the procurement of a home or the anticipation of a vacation, often become overshadowed by the immediacy of financial obligations. This illustrates the profound reach of medical debt on an individual's holistic well-being.

Global Insights: International Best Practices

Upon broadening our perspective to a global scale, a distinctive narrative emerges. Numerous countries have instituted comprehensive medical benefits for their military personnel. These established systems, characterized by their proactive strategies and extensive coverage, set benchmarks of excellence.

Given these international precedents, it may be prudent for the U.S. to evaluate and discern applicable lessons from these best practices. Such a comparative analysis is valuable for refining domestic approaches to military medical benefits.

Marching Forward: Advocacy And Initiatives For Change

Significant developments are underway in the evolving landscape of the medical debt crisis for military families. Current legislative agendas feature multiple proposals aimed directly at alleviating this pressing concern. Concurrently, grassroots movements and dedicated organizations fervently mobilize and advocate for systemic changes and reforms.

For individuals and entities deeply vested in this issue, ample opportunities exist to engage, support, and drive impactful transformations in this crucial arena. The confluence of these efforts underscores a proactive approach toward addressing the challenge at hand.

Conclusion

In conclusion, it is imperative to underscore our shared responsibility. Addressing the challenge of medical debts within the military goes beyond mere policy adjustments. It is a matter of ensuring that those who have dedicated their lives in service to the nation are not disproportionately burdened upon their return. As a cohesive society, extending our unwavering support and commitment to these individuals is commendable and an essential duty.

Read More:

How To Choose A Funeral Director?

How to Get Low Cost Life Insurance for Seniors?

5 Factors to Consider in Choosing the Right Floor Colors

The stock market is one of the investment platforms that readily come to mind when (especially) new investors think about investing. The truth is that this investment platform promises a lot. This is the reason many people take this investment route.

Be that as it may, you need to know that this investment platform has its few downsides. However, they are few enough to have caused many people financial wrecks in the past. The point is not to discourage you from investing in the stock market.

Trading commodities can be a great decision if you are looking to diversify your portfolio. Historically, precious metals like gold and silver have been tried-and-tested safe investment options as far as traders are concerned. You can get in touch with a leading gold trading broker to evaluate your options and then proceed accordingly by trading these commodities.

However, it is about opening your eyes to some of its dark sides and making sure you see the need to diversify your investments. This way you can make the most of many investment platforms or make sure you are not completely at a loss if the stock market has problems.

For those that need to better understand the possibility of the stock market crashing, you can visit: https://en.wikipedia.org/

You would discover that regardless of where they are situated, no stock market is completely immune from a crash. Investors in places like the United States, the United Kingdom, China, Brazil, EU Nations, Dubai, Japan, South Korea, and many other places have had this experience.

It is for this reason we all need to equally consider investing in other profitable assets as well. On this note, this article will shed some light on gold and silver investment.

The ways this can play out and a few other things will be explained here. The information here is very important and so you are advised to keep reading. You should also pay rapt attention as you do so.

Gold or Silver – Which Should You Invest in?

For the record, both precious metals are not the only options that can be considered by those hoping to make the most of the precious metal market. However, both are unarguably the most common options for precious metal investors.

Other than this, some of the details discussed concerning both precious metal assets are equally applicable to others. Having established this, the million-dollar question on many people’s minds is “should I invest in gold or silver?”

There are many things you need to consider to make the proper decision in this regard. One of them is something known as the gold-silver ratio.

This is about using the value difference between both precious metal assets to make informed decisions as an investor. Fortunately, there is always a clear figure of this ratio to help people make the right choice. You need to make your decisions based on this ratio amongst other things. This is so that:

You choose precious metals based on their prospects

You get your assets at a market valuation that is fair

Your assets will not be undervalued when it is time to liquidate the assets

These are some of the basic reasons you should take this ratio seriously as there are a few other reasons. Against this backdrop, you should also make sure you are working with real-time information.

This is to be certain that your investment decisions are well informed. If you would like to know more about the gold-silver ratio (especially how it is calculated), you can read this article.

Investing in Gold and Silver

Some similarities come with investment in gold and/or silver. One of them is that they share the same investment methods for the most part.

So, this is valuable information for those planning to invest in silver, gold, both precious metals, and even a few other precious metals. Having established this, some of the methods that can be considered include:

1. Bullion Purchase

There are a few precious metal forms that would pass as bullion. However, the underlying factor here is that the precious metals are gotten, sold, and valued based on their weight. This is unlike what is obtainable with collectibles and special precious metal coins.

Speaking of bullion, they would either be offered as bullion coins or bars. The latter usually weighs one ounce and its valuation is based on this. On the other hand, the former weighs a lot more. This is no less than 400 ounces.

To invest in gold and silver using this method, you have to work with a precious metal exchange company. Many service providers are in this business. Some of the very common ones include Money Metals, JM Bullion, Vaulted, and a host of others.

It is very important that your chosen precious metal exchange company ticks all the right boxes. This is in terms of credibility, impressive track record, and a long list of other important things. You are advised to get a full review from a credible review platform(s) to make the right choice.

2. Gold IRA

The Internal Revenue Service is heavily involved in formulating tax laws and seeing to it that they are implemented in this country. This is especially at the federal level.

You should also know that this body is also actively involved in regulating the IRA scheme. The IRA scheme offers a lot of tax benefits to account holders and the good news is that there is an IRA plan that allows people to invest in precious metals.

The truth is that there are only 4 precious metal assets that the system allows account holders to invest in. These are gold, silver, platinum, and palladium.

You are advised to understand the rules set by the IRS as regards investing in precious metal assets. These are especially rules that center on withdrawal of precious metal assets, storage, eligible forms of precious metals, approved purchase techniques, and so on.

3. ETFs

This is an investment option that is quite popular. This is especially as it concerns investment in the stock market. The good news is that the Exchange Traded Fund (ETF) system is not restricted to the stock market.

You can also make the most of the precious metal market using this system. Other than the bullion purchase method discussed above, this one would not require handling the assets physically.

Frankly, this is one of the advantages of this silver and gold investment method. For more on this subject, you can visit: https://www.businesstoday.in/commodities/story

Conclusion

We have discussed a few things you need to know as someone hoping or planning to invest in silver or gold. You should also know that some of the information here will help you invest in other precious metal assets properly. So, you are advised to make the most of these details going forward.

Read Also:

5 Reasons Why Bitcoins Are Considered Reliable Investments

5 New Assets To Diversify Your Investments In 2021

Top 5 Investment Decisions You Need To Make In Your Thirties

Your attendees will have the ability to make payments and donations at any time of day or night thanks to the online payment management system. A system that is PCI-compliant will simplify the process of receiving payments, balancing transactions, managing refunds, addressing chargebacks, and maintaining merchant accounts.

Your attendees will have the ability to make payments and donations at any time of day or night thanks to the online payment management system. A system that is PCI-compliant will simplify the process of receiving payments, balancing transactions, managing refunds, addressing chargebacks, and maintaining merchant accounts.

If you've gotten this far in your quest to become a payment facilitator, you'll soon reach a crossroads. However, in this crucial stage, you must choose between developing your own infrastructure from the ground up or integrating another party's in order to onboard and serve your sub-merchants.

If you've gotten this far in your quest to become a payment facilitator, you'll soon reach a crossroads. However, in this crucial stage, you must choose between developing your own infrastructure from the ground up or integrating another party's in order to onboard and serve your sub-merchants.