Published on: 04 August 2021

Last Updated on: 10 January 2025

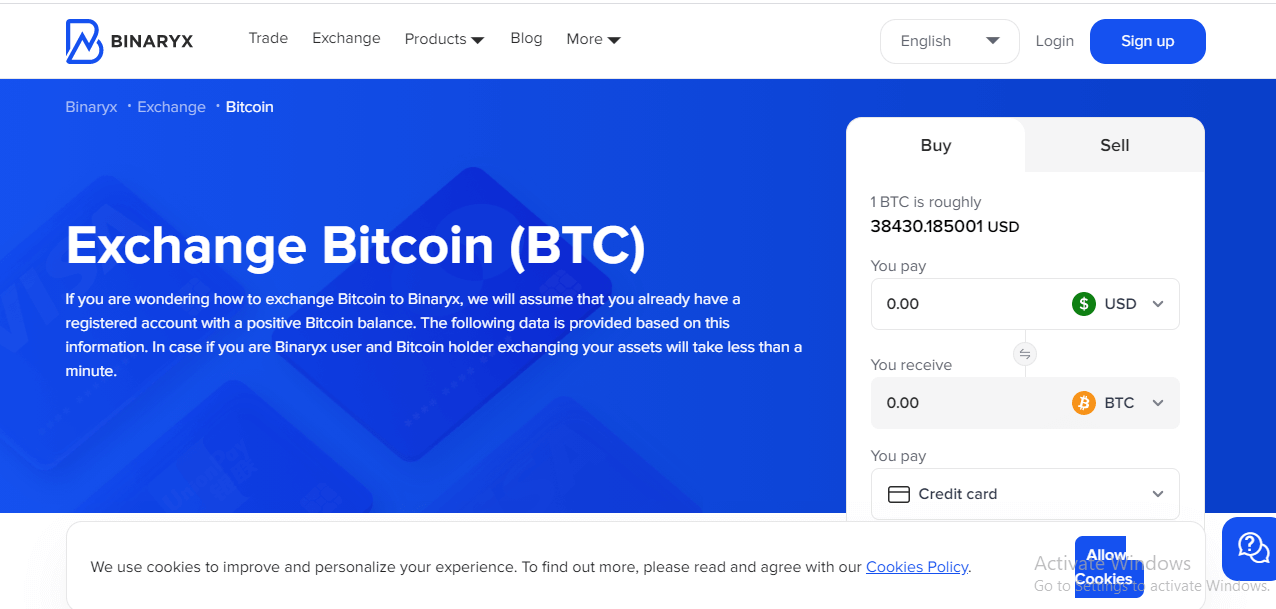

Binaryx is one of the best digital asset trading platforms that has emerged in the last few years. It offers a number of simple, progressive, and functional solutions for everybody who wants to exchange bitcoins or buy and sell digital and fiat currency. The cryptocurrency exchange was created in 2019, with headquarters in Tallinn. It is authorized by law and has a European legal license for trading and other crypto operations. The scalable and intuitive interface of the trading and exchange modules delivers convenience for every user, who can exchange bitcoins or other assets from the comfort of their home or office.

The Key Features Of The Binaryx Cryptocurrency Exchange

Often, the bitcoin and the forex traders can not find an authentic platform to exchange Bitcoin. The cryptocurrency as the platform’s authentication and trustworthiness makes the platform unique and reliable. While you are doing the cryptocurrency exchange, the requirements of the authentic platform are high.When you are doing transactions on many types of cryptocurrency, it is quite absurd that you are going to use individual platforms for the individual types of cryptocurrency. The Binaryx is the all square platform.Binaryx suits both novice traders and savvy investors. Go to https://www.binaryx.com and start making money on trading and exchange right now!

The project’s main idea is to implement a trading platform for customers who want to exchange money for bitcoins or sell and buy digital assets, regardless of their experience or expertise.

This is a comprehensive project with a smooth-running ecosystem incorporating trading services, educational products, and opportunities for making money on crypto skills. The cryptocurrency exchange offers a range of useful tools and provides broad functionality.

Platform users appreciate a user-friendly website, profitable trading terms, professional support, high security, and extensive functionality. Binaryx means good trading limits, low commissions, minimum registration requirements, and the availability of the exchange bitcoins process for everyone.

The developers of the cryptocurrency exchange, inter alia, are constantly working on improving the current offers to provide the best solutions to exchange bitcoins and more.

Step-By-Step Guide: How To Sell And Exchange Money For Bitcoins

Are you a beginner in cryptocurrency trading? Take a look at the step-by-step guide to perform the cryptocurrency exchange in the Binaryx. This platform is quite a comfortable place for beginners. Follow these steps and start with the registration.

1. Registration:

The registration process is twofold — you can log in via your social media account or create an account using your email. Whichever method you choose, following the registration process, you will be able to sell, buy, exchange bitcoins, and perform any trading operations.

2. Verification:

To complete registration, you must go through the basic stages of verification. First, it’s confirmation of your email. Then, you will need to undertake extended verification to trade and exchange money for bitcoins without any restrictions.

3. Account replenishment and withdrawal of funds:

Replenishment of the cryptocurrency exchange account is carried out in wallets. After crediting money to your wallet, you can move on to trading or exchange bitcoins operations.

4. Trade and exchange money for bitcoins:

Binaryx has a great multifunctional trading terminal and exchanger that allows you to buy or sell coins quickly.

Conclusion:

For bitcoin traders, secure platforms are the only authentic platform to exchange bitcoins. When you are using this platform, you will understand how the platform is made easy. Join Binaryx and experience all the benefits of this advanced and innovative cryptocurrency exchange!Read Also:

Content Rally wrapped around an online publication where you can publish your own intellectuals. It is a publishing platform designed to make great stories by content creators. This is your era, your place to be online. So come forward share your views, thoughts and ideas via Content Rally.

Passive income is the lifeblood of any investor's portfolio. It provides you with a reliable and consistent stream of income while you take some time away from work.

Having a passive income stream is a great way to supplement your existing income or build a retirement fund. As tax season approaches, now is the time to evaluate your current situation and determine if you are taking advantage of this amazing opportunity.

Checkout Five Prime Ways Of Passive Income You Need To Learn Now

Here are a few examples of passive income sources you should explore now:

1. Real Estate Investments

Real estate investments can be a great way to generate passive income. Most real estate investments are done through rental properties. You buy a property and then rent it out for a monthly fee. Property owners may be able to collect enough rent to cover their mortgage payments, leaving them with a steady stream of income.

Real estate investors may also want to consider buying pre-construction developments and flipping houses. With pre-construction development, you can purchase a property before it's built and then sell it for a profit when it's done.

Flipping houses involves buying a home and making improvements to it before reselling it for a higher price. Both pre-construction developments and house flips can yield considerable profits in a short amount of time.

Real estate investors should also look into commercial real estate investments. This type of real estate involves investing in multifamily, industrial, and retail properties. Owning commercial real estate can be a great way to generate income as well as appreciation when done right. Investors may also want to consider investing in REITs, or real estate investment trusts.

REITs are investments that pool a variety of real estate assets and offer investors exposure to the real estate market without owning physical properties. Real estate investments come with the potential for great rewards but also come with their own unique set of risks. Investors should consider consulting a financial professional before pursuing a real estate investment.

2. Dividend Investing

Dividend investing is another popular way to generate passive income. When you invest in a company through a stock, you become a shareholder and may receive regular dividend payments from them. Dividend payments can vary from company to company and are a great way to make a reliable income without having to actively manage any assets.

Dividend payments are usually paid quarterly, but some companies can pay them more or less often. The amount of the dividend payment you receive is dependent on the number of shares you own, the type of stock you purchase, and the amount of capital growth the company's assets have achieved.

In addition, dividends are also paid in proportion to how long you've owned the stock. Dividend investing can help to diversify your income stream and reduce the volatility of your investments. Dividend investing also has tax advantages and can be used to help you reach your financial goals.

3. Investing in Index Funds

Index funds are a type of mutual fund that tracks a particular market index. By investing in these funds, you’re basically buying an entire portfolio of stocks without having to actively pick and choose which ones to invest in. Index funds offer a great way to get passive income while diversifying your portfolio.

Index funds also typically have lower management fees than actively managed funds, which helps reduce the overall expense of your investments. The main benefit of investing in index funds is to get exposure to the broader stock market without having to pick individual stocks.

By following an index, you benefit from its diversification and protection against individual stock risk. Additionally, indexes often have a good return on investment and tend to outperform actively-managed mutual funds over time.

4. Peer-to-Peer Lending

Peer-to-peer lending is a type of lending that takes place between two individuals. It involves lending a certain amount of money to someone else and then receiving regular payments in return. Peer-to-peer lending is a great way to generate passive income without putting your money at unnecessary risk.

It is often used to finance investments and small businesses. As the lender, you can decide how much to loan, the repayment terms, and the interest rate. Peer-to-peer lending helps to diversify your investments and can provide you with returns and future income.

5. Online Businesses

Finally, starting an online business can be a great way to generate passive income. Whether it’s an e-commerce store, a blog, or a subscription service, an online business can be scaled up to generate a significant amount of income. Plus, it can be done from the comfort of your own home.

An online business can be a great way to create a passive income stream, as it can be scaled up over time to generate more revenue. With an online business, you have the potential to reach a wider audience from all over the world, as the internet doesn’t have any geographical restrictions.

You’re also able to work from the comfort of your own home, set your own hours, and have the flexibility to work when and where you want. Depending on the type of business you set up, some possible revenue streams include selling products, offering services, advertising, membership fees, and affiliate marketing.

Setting up an online business takes time, dedication and effort, and a solid business plan. It’s also important to have a clear understanding of local and international laws, taxes, and regulations so you remain compliant.

No matter which type of passive income you choose to pursue, make sure you understand the ins and outs of government regulations around the area. During tax season, it is important to ensure you complete all the required paperwork and pay taxes on any income you might generate.

It is also important to ensure that any sources of passive income are reported on your paystub, otherwise, you could end up owing a lot of money in unexpected taxes.

By learning what passive income sources are available, you can start to build a reliable and consistent stream of income quickly and easily. Explore the different options outlined above and determine what works best for you and your financial situation. The rewards can be great and you'll thank yourself in the long run.

Read Also:

How To Choose A Great Managed Fund

4 Fun Jobs After Retirement That Offer You a Monthly Income

A Beginners Guide to Investing: Getting Started in 8 Simple Steps

The traditional investment model is a flawed system, an old dinosaur that needs to evolve.

It’s time we reevaluate the conventional wisdom surrounding investments, which is overly fixated on businesses that are already successful and tragically shortsighted when it comes to companies teetering on the edge of growth.

In traditional investing, there’s an unspoken rule: the golden ticket to getting funding isn’t innovation or potential but a proven track record of making at least $10 million. This is a narrow-minded approach that does nothing more than stifle the very heart of our economy—small businesses.

Introducing sweat equity

Eight-figure entrepreneur, growth mentor, and innovative investor Tamara Loehr (www.tamaraloehr.com) bring a breath of fresh air to the world of investing. She’s not your usual investor who waits for businesses to reach millions before swooping in.

Instead, she actively seeks out businesses with potential and partners with them by investing her expertise and services to help them achieve growth and significant returns.

She calls this sweat equity investment, a unique model that’s a game-changer for businesses. Tamara doesn’t merely provide financial backup; she rolls up her sleeves and brings a wealth of expertise, strategic vision, and creative solutions to the table.

It’s a holistic approach that not only increases the likelihood of success for the businesses she invests in but also amplifies the potential returns for both the entrepreneur and herself.

By focusing on small businesses and collaborating with them closely, Tamara is paving the way for a new era of investing that champions small businesses and fosters a more inclusive and dynamic business landscape.

What is sweat equity?

Sweat equity is a unique investment model where investors exchange their expertise, resources, and time for equity in a business. Tamara came up with this innovative approach to investing after seeing how traditional methods often left entrepreneurs struggling to repay loans or lose equity in their businesses.

In this model, instead of investing cash, investors offer services to companies in exchange for a stake in their business. It's a win-win situation for both parties, as businesses receive the much-needed resources to grow, while investors gain a stake in a growing business.

Why sweat equity works

Sweat equity investment offers a unique and innovative approach to investing that can provide a range of benefits for both investors and entrepreneurs. If you're a creative investor looking to explore new investment opportunities, sweat equity investment is worth considering.

Entrepreneurial access to expertise

One of the key advantages of the sweat equity investment model is the access to expertise it provides to entrepreneurs. Founders have a strong vision and passion for their business but may lack skills or experience in areas such as finance, marketing, or operations. By partnering with a sweat equity investor with expertise in these areas, businesses can leverage this knowledge and experience so they can succeed faster.

Sweat equity investors like Tamara are experienced business owners who have a track record of building and scaling successful companies. They are looking for new investment opportunities that align with their expertise and interests and are willing to offer their skills in exchange for equity. This type of partnership allows entrepreneurs to access the expertise they may not be able to afford to hire on their own.

Entrepreneurs also gain access to an investor’s connections. These investors often have a vast network of contacts that can be beneficial to the business, including suppliers, customers, and other professionals in the industry.

Sweat equity investors also have a vested interest in the success of their investments. They are not just passive investors but active partners who are invested in helping their partners achieve their goals. This means that they are likely to be more involved in the day-to-day operations of the business, offering guidance and advice as needed.

Capital conservation

Instead of pouring all their capital into hiring consultants or buying equipment, businesses exchange equity for the expertise and resources they need. This approach can be particularly useful for startups and small businesses that may have limited financial resources.

When entrepreneurs team up with sweat equity investors, they’re essentially receiving support and guidance in exchange for equity. By doing so, they’re preserving capital and freeing up funds that can be reinvested in other areas of their business. This can be a game-changer, especially in the early stages of the business when cash flow is often a major challenge.

The value of sweat equity extends far beyond the immediate financial gain. Entrepreneurs gain access to experts who are invested in the success of their business and who can help build and grow the company over time. By leveraging sweat equity, they’re setting themselves up for long-term success and sustainability.

Risk mitigation

When it comes to investing, risk is always a factor to consider. However, the risk can be mitigated with sweat equity investments. Investors and entrepreneurs share the risks of a sweat equity investment, thereby reducing the financial burden of starting, growing, and investing in a business.

This shared-risk approach provides a safety net for entrepreneurs who may not have the financial resources to weather unexpected expenses or a downturn in the business.

And because the investor is a partner and has a vested interest in the success of the business, they are more willing to provide support during difficult times.

Overall, the risk-sharing associated with the sweat equity model can help entrepreneurs avoid bankruptcy or failure and increase their chances of success.

Long-term commitment

One of the most compelling reasons for exploring sweat equity investment is the long-term commitment it demands from both the entrepreneur and the investor.

In a traditional investment model, investors are primarily focused on achieving financial returns and may not have a vested interest in the long-term success of the business.

With sweat equity investment, both parties have a shared interest in the success of the business. The investor is contributing not just financial resources, but also expertise and guidance, which makes them invested in the company's future. This commitment from the investor can provide stability and security for the entrepreneur, who has a partner who is as committed to the business's success as they are.

This shared commitment also means that both parties are willing to work together through challenges and changes, adapting and evolving as needed. In essence, sweat equity investment creates a partnership based on a mutual commitment to the business's long-term success.

This long-term commitment is especially valuable for creative investors who are looking to invest in innovative, high-potential businesses. They have the opportunity to be part of something they believe in and help guide the company toward its full potential.

Credibility booster

Sweat equity investment is not just a way to conserve capital or mitigate risk, but also a chance to enhance an entrepreneur’s credibility. Customers and investors are more likely to do business with a company that has an experienced partner behind it.

This type of partnership can lead to a reputation boost that ultimately results in more opportunities for growth and expansion.

Aligned goals

With sweat equity, the investor becomes a stakeholder in the business and has a personal interest in seeing it succeed. This shared interest ensures that both parties are working towards the same objectives and helps create a more collaborative and supportive relationship.

When investors are only focused on financial returns, there can often be a misalignment of priorities with the entrepreneur. This misalignment can lead to conflict, mistrust, and a breakdown in the working relationship. With sweat equity, however, both parties have a vested interest in the success of the business. This shared interest can foster a strong sense of trust and cooperation between the two parties.

Also, when the investor is invested in the long-term success of the business, they are more likely to stick around and provide ongoing support and guidance to the entrepreneur. This can help the entrepreneur navigate the challenges of growing a business and accelerate the path to success.

Value-added mentorship

One of the key benefits of the sweat equity investment model is the personalized mentorship that investors inevitably provide to entrepreneurs.

For many entrepreneurs, starting a business can be overwhelming, and they may lack the necessary experience in certain areas of the business. This is where mentoring by a sweat equity investor becomes crucial. With their guidance and support, the entrepreneur can avoid costly mistakes and take the right steps to grow their business.

The mentorship also provides entrepreneurs with an outside perspective and a fresh set of eyes. This can help identify areas of improvement and opportunities for growth that may have gone unnoticed. Through regular communication, investors can hold entrepreneurs accountable and help them stay on track with their goals.

Ultimately, mentoring is a win-win situation for both parties. The entrepreneur gains valuable insights and guidance, while the investor can contribute to the growth and success of the business. With the right mentorship, entrepreneurs can take their businesses to the next level and achieve long-term success.

Takeaway

Sweat equity is a game-changing investment model that provides a host of benefits to both investors and entrepreneurs.

Tamara’s approach, which focuses on creating a long-term relationship between the investor and the entrepreneur, allows for a unique level of collaboration and expertise-sharing that traditional investment models cannot provide.

Not only does sweat equity offer a way for entrepreneurs to conserve capital and mitigate risk, but it also leads to an alignment of goals between business and investor.

As an investor, it's essential to explore this innovative approach to investing and consider incorporating it into your investment strategy. By doing so, you’re not only investing in a business but in the potential growth and success of the entrepreneur themselves.

Read Also:

A Beginners Guide to Listed Investment Companies

How to Successfully Turn Around Struggling Companies

Is Investment Managers A Good Career Path In 2021?

As a small business, you’ll want to make it your priority to begin creating revenue immediately when starting up.

This can be difficult, but it will set your company in good stead for what the future brings. Ultimately, you cannot rely on funding.

Plus, whatever you have in your pocket to get to where you not only want to be but also need to be. If you’re a small start-up, continue reading to find out four ways you can improve your Startup Revenue.

Try to Have Immediate Cash Flow

Whilst it is useful having funding to create and attempt to grow your start-up, this money can be over rather quickly. Especially when you work out what you intend to do with it.

That said, it is impossible to continue as a small business without attracting immediate cash flow into the company.

Pumping money into the business earlier on will provide you with a great immediate start-up. However, it is essential that you make sure this money is spent on the right things and not useless items. It is possible to invest, too, but your investments are not wholly reliable.

Therefore, experts recommend that you attempt to sell and provide your goods and services. This is from the get-go to have some form of cash flow arriving promptly.

Have Business Insurance

Another practice that will improve your revenue as a small business start-up is investing in business insurance. For some sectors, it is a legal requirement to have business insurance.

Even experts generally recommend that business owners invest in it anyway.

Your certificate of insurance It is a great form of protection for your business and employees.

This insurance could improve your startup revenue as it could take care of your business. It could also act as a safety net if something was to go wrong.

For example, if your premises were broken into two weeks into the operation, the insurance would provide financial compensation.

Recruit within Your Means

Recruiting and hiring staff as a small business can be a daunting task, especially if it’s the first time you’ve tried it.

It is important that you don’t attempt to run the entire business yourself. This is because you’ll soon realize that your products and services suffer as a result.

Hiring and retaining staff within your means is a reasonable way to improve startup revenue.

Use Social Media

The growth of social media has been an excellent tool for all businesses. It has even been a lifeline for smaller businesses.

This is because these businesses essentially don’t have the funding to invest in digital marketing. Therefore, we need to rely on free forms of advertising. Social media being the greatest of all!

As a start-up, you’ll save money by marketing yourself, and you’ll also increase revenue by connecting with a large audience online. This way, you’ll gain rapport with customers and clients as well as make money.

Consider these tips to improve your startup revenue from the get-go.

How to Improve your Cash Flow as A Startup

Starting a business is all good, but if you don’t have cash flow — a steady flow of incoming cash — your business will go belly up.

No matter how great the business idea or product is.

Just Start Selling!

It will never be the perfect time to finally launch that product or service and begin selling!

You will have to just bite it and do it for once!

You won't be able to start generating revenues if you just keep thinking about how to bring the money!

The key to immediate cash flow is to start selling your products or services as soon as possible. You don’t have to wait until everything’s perfect before you begin making sales.

Whether it’s pre-orders, minimum viable products, or service contracts, find a way to get money coming in right away.

Not only will this help you generate revenue faster, but it will also validate your business concept with real paying customers.

Watch Your Expenses

Every dollar a startup spends should be spent in expectation of ROI. Spend to grow and spend as late as possible, never earlier.

Don’t spend money on anything that doesn’t have a direct impact on your growth – especially when you are just starting.

Keep a Close Eye on Your Financials

Review your cash flow statement regularly so you know who is paying you and where your money is going.

Then, use that information to help you make better decisions about your spending, pricing, and growth strategy.

Not keeping an eye on this will cause unexpected shortages of cash flow but, more importantly, can put you in a financial bind.

To Wrap it Up!

To be a successful startup entrepreneur, you must constantly improve your cash flow.

This means selling as early as possible, possibly before you are ready, managing your expenses against sales, offering the right payment terms to customers, and paying close attention to accounts receivable.

Read Also:

7 Growth Hacking Ideas that will Boost your Startup

Best Server Management Tips for Startups

Useful Marketing Tips for Startups

Often, the bitcoin and the forex traders can not find an authentic platform to exchange Bitcoin. The cryptocurrency as the platform’s authentication and trustworthiness makes the platform unique and reliable. While you are doing the cryptocurrency exchange, the requirements of the authentic platform are high.

When you are doing transactions on many types of cryptocurrency, it is quite absurd that you are going to use individual platforms for the individual types of cryptocurrency. The Binaryx is the all square platform.

Binaryx suits both novice traders and savvy investors. Go to https://www.binaryx.com and start making money on trading and exchange right now!

Often, the bitcoin and the forex traders can not find an authentic platform to exchange Bitcoin. The cryptocurrency as the platform’s authentication and trustworthiness makes the platform unique and reliable. While you are doing the cryptocurrency exchange, the requirements of the authentic platform are high.

When you are doing transactions on many types of cryptocurrency, it is quite absurd that you are going to use individual platforms for the individual types of cryptocurrency. The Binaryx is the all square platform.

Binaryx suits both novice traders and savvy investors. Go to https://www.binaryx.com and start making money on trading and exchange right now!

Are you a beginner in cryptocurrency trading? Take a look at the step-by-step guide to perform the cryptocurrency exchange in the Binaryx. This platform is quite a comfortable place for beginners. Follow these steps and start with the registration.

Are you a beginner in cryptocurrency trading? Take a look at the step-by-step guide to perform the cryptocurrency exchange in the Binaryx. This platform is quite a comfortable place for beginners. Follow these steps and start with the registration.