Published on: 10 December 2020

Last Updated on: 11 September 2024

Being a real estate agent is already a tough job. With so many agents in the market, competition is fierce. Agents must do their best to win market share.However, in today’s market, traditional direct marketing strategies are less effective. Hard-earned cash is spent on Facebook and Google ads, yielding little return. The ROI of direct marketing strategies is increasingly unsatisfactory.This decline doesn’t appear to be a one-time issue. A meaningful trend seems to be emerging: the audience is overwhelmed with too many marketing messages.They’ve started ignoring repetitive, uninspiring ads. It’s frustrating, especially for new agents lacking the advantages of word-of-mouth and referrals. Yet, repeating old strategies won’t fix the problem.To turn this around, agents should think from the audience’s perspective.

The Root of the Problem: Bad Content

Real estate, like any business, is flooded with repetitive marketing messages. Most agents claim to be the best but offer the same content. A quick glance at social media and Google ads reveals most ads focus on agents themselves. Few consider what clients truly need.In 1996, Bill Gates said, "Content is king." He saw the internet’s potential early on, predicting content would be its foundation. Today, content indeed reigns. Audiences are tired of ads offering nothing new. Content is the key to standing out. But creating content isn’t enough creating great content is what matters.What is great content? Simply put, it’s what your audience is searching for. It addresses their needs and concerns. Real estate can be complex for homebuyers and sellers. They have questions and want expert guidance. Agents who address these concerns become the trusted go-to experts.

Videos, Videos, Videos

We can’t stress this enough. Watching videos is easier than ever thanks to faster internet speeds.Millions of videos are shared daily across platforms like Facebook, Instagram, and Twitter. YouTube, the largest video platform, makes watching content effortlessly.But creating videos is harder than watching them. The valuable content mentioned earlier is best delivered in video form. Is a bad video better than none? Absolutely not. In real estate, reputation and brand image are delicate. Poor-quality videos can do more harm than good.

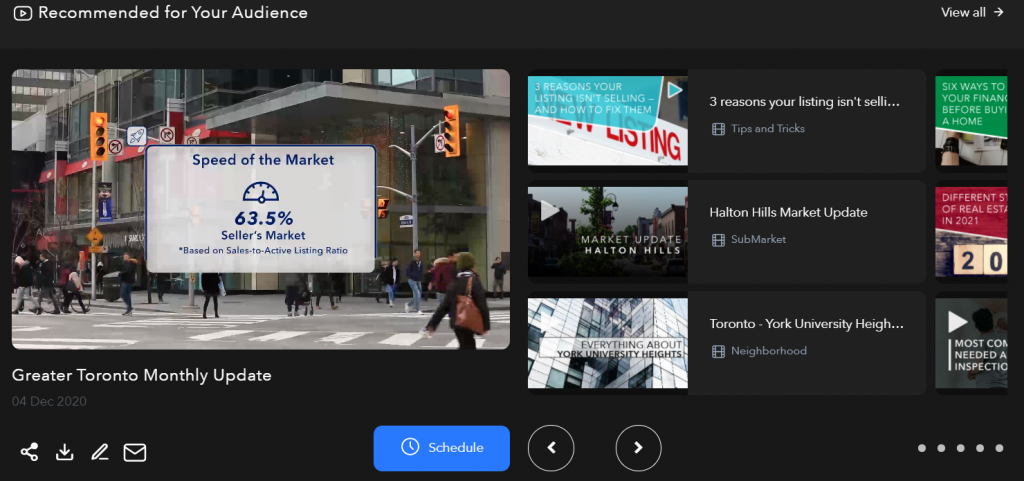

roomvu market update videos

Since video production is challenging, many agents avoid it altogether. But this means missing out on significant benefits. With a little research, agents can find tips for creating their own videos or ideas for content. Hiring a professional real estate video creator is another option. Though it may seem like an extra expense, the ROI is worth every penny.

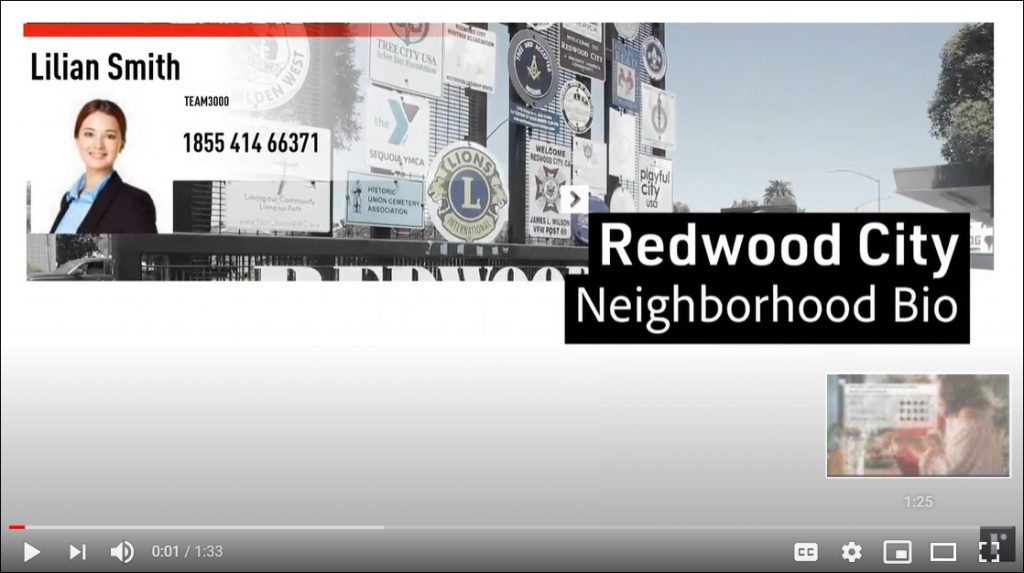

roomvu neighborhood bio videos

Social Media, Automated

Social media is one of the best channels for generating real estate leads. Features like Instagram Live help agents connect with larger audiences. If you have the time, skill, and patience to manage several social media accounts, then go for it. But most agents, with their busy schedules, struggle to do so.Success on social media requires consistency and engaging in valuable content. Many agents shy away from it due to a lack of time, skills, or content. Yet, they can still reap the benefits by using automation tools. Platforms like Roomvu offer social media automation services, including content creation and scheduling.Roomvu’s service does all the heavy lifting, even providing a free content calendar. Agents simply connect their accounts, choose the right content from Roomvu’s content factory, and let the automation handle the rest.

roomvu social media calendar

Get Creative with Your Marketing Content

Marketing in real estate doesn’t have to be boring or repetitive. Instead of focusing on your achievements and credentials, dive into content that matters to your audience.Share tips for first-time homebuyers, discuss market trends or answer common questions people have.Clients aren’t looking for just another agent—they’re looking for a guide they can trust.Agents who focus on educational content become resources clients naturally turn to.When you regularly offer valuable insights, clients see you as more than a salesperson—they see you as a trusted advisor.A key tip here is to mix up your content style. Don't just rely on blogs or posts; experiment with infographics, podcasts, and especially videos.

Build Relationships, Not Just Sales Pitches

Social media is a fantastic tool for connecting with potential clients. But it's not about blasting listings or boasting about recent sales. It's about engagement as well!Whenever you get time, reply to comments, answer questions in DMs, and participate in discussions. After all, the goal is to build relationships, not just push sales.Automation tools can help keep your content consistent, but don’t let them make your approach robotic.Take time to interact personally whenever possible. Even if it’s just a quick response to a comment, it shows you’re approachable and genuine. People want to work with agents who care, not those who just see them as numbers.

The Power of Consistency and Patience

Real estate success rarely happens overnight. Building a brand, growing a following, and gaining trust takes time.Consistency is everything. Keep posting, keep sharing values, and keep interacting with your audience. Don’t get discouraged if the results aren’t immediate. The key is to stay persistent.Creating great content regularly might feel overwhelming, but it’s worth the effort. The agents who succeed are the ones who stick with it, even when it feels like no one’s paying attention.

Final Words

Agents can’t afford to stick to outdated methods. Traditional direct marketing strategies are failing because they lack value.People no longer click on ads that only make empty claims. The problem isn’t advertising itself—it’s the lack of valuable content.Agents should adopt a fresh approach to marketing. Focus on being a helpful expert who shares useful information.Address your audience’s needs and concerns with insightful, valuable content, preferably in video form. This strategy requires patience and consistency, as building a community takes time.Success in real estate’s competitive market comes from putting customers first. Understand their needs and concerns rather than just promoting yourself as the best agent.Read Also:

Content Rally wrapped around an online publication where you can publish your own intellectuals. It is a publishing platform designed to make great stories by content creators. This is your era, your place to be online. So come forward share your views, thoughts and ideas via Content Rally.

Deciding to buy a home warranty plan is a smart move for homeowners. However, with so many providers and options out there, picking the best one might feel overwhelming. Luckily, there are many things a homeowner can research to ensure they select a policy that will serve them well.

Home warranties are different than insurance. Home warranty plans are supplemental contracts that cover common household repairs. Policyholders have monthly or annual premiums and pay a discounted rate for qualified service calls. Here's what potential buyers need to ask when looking at homeowners' warranty policies.

What Does The Plan Cover?

Not all home warranties are the same. One plan might cover household appliances, but another might include systems. Air conditioning coverage isn't always included or might only be offered as an add-on. The same goes for refrigerators. Systems include electrical, plumbing, and water heaters, but once again, not all policies cover every system. Optional coverage options could include sump pumps or septic tanks.

Before signing on the dotted line, double-check what the preferred plan covers. Take inventory of all appliances, and compare the list to several policy options. For example, a built-in microwave might fall under optional coverage. Selecting the right amount of coverage now will save money down the road.

How Much Is The Premium?

Sticking to a budget when shopping for a home warranty is important. The cost depends on a number of factors. High-coverage plans with additional add-ons will be more expensive than a standard policy. That's why asking about the price before picking a plan is essential.

The premium is how much the policyholder pays for the plan. Some companies charge a lump sum annually, while others divide the premium into monthly payments. It's also wise to inquire about any deductibles required when making a claim.

How Long Is The Waiting Period?

Most home warranty providers have a mandatory waiting period before paying benefits. The most common is a 30-day period. Further, a coverage gap between policy renewals might trigger another waiting period. Before signing the contract, find out when benefits will be in place.

What Are Current And Past Customers Saying?

The goal of a home warranty agent is to sell a policy. Of course, they will sing the highest praises about their company to lure in new customers. However, are they telling the complete truth? Instead of believing an agent, find out what other customers have to say.

Customer reviews are the best way to get an honest, blunt opinion about a home warranty provider. Read all the reviews, including the good and the bad. What compliments does this provider receive the most? What are their weaknesses? Online home warranty reviews help homeowners make a more informed decision.

What's In The Fine Print?

Home warranty plans are long and often hard to read. However, buyers need to read every word, including the fine print. Look for any exclusions, such as pre-existing wear, cosmetic damage, or manufacturer warranties. The right plan will be upfront and easy to understand.

Get A Quote And Repeat

Home warranties save homeowners a bundle on appliance and system repairs. However, picking the right one takes time, research, and effort. Ask all the questions mentioned above when comparing plans, request a quote, and repeat the process with another provider. Doing so will ensure the warranty you ultimately select serves you well into the future.

Read Also:

Home Improvement Hacks to Add to Your Space

Ideas for Modern Flooring Designs for Home Improvement Plans

6 Interior Design Tips to Make Your House a Home

The prospect of buying a new home for the first time is indeed a very special one. You are excited at owning a valuable piece of asset that you will call your home. For first-time buyers, getting the right property at an attractive price is a top priority.

As against someone who regularly invests in real estate and understands the ins and outs, first-time buyers stand at a disadvantage. The real estate market is a very dynamic one. There are so many things that can affect the influence the price of a home.

This is why the importance of a good realtor that can help guide them in the right manner is critical. From an understanding of the various neighborhoods to locating homes within a budget, a good realtor can be an asset that can make your first-time home buying experience a happy one!

In this article, we are going to help first-time homeowners pick out the best realtors for their specific conditions. If you are someone that is looking to buy a new home for the first-time, this article will help you in multiple ways.

The Problems first-time homebuyers Experience in the Real Estate Market

In this section, we are going to look at some of the key problems first-time homebuyers face when looking at the real estate market-

Budget Constraints-

Yes, addressing the elephant in the room first. Budget constraints are something that almost a majority of homebuyers need that is affordable, within their budget, and will rise in value in the near future.

Trust Issues and Worries-

In a market where everyone is running after their own interests, trusting someone can be tough. This is why first-time homebuyers are extra cautious before moving forward. This sometimes costs them great deals in real estate.

Network and Connections-

Buying a home does not only mean working with a realtor. It involves working with legal experts for the property’s paperwork, getting help from loan agents at banks, and engaging contractors. Sometimes, all this becomes too much.

Decision-Making Troubles-

Investing so much money in a property is a decision that requires a lot of courage. Second-guessing the decision to invest makes first-time homebuyers develop cold feet even when a great deal is staring them in the face.

Understanding of Neighbourhoods-

Most of us feel comfortable in staying close to our communities and groups. Given the recent spate of violence and societal troubles, first-time homebuyers are conscious of their family’s

These are some of the most common and basic problems that first-time homebuyers experience when making decisions on real estate.

5 Important Things to look at in a Realtor before you hire them

In this section, we are going to let first-time homebuyers in on a secret. By pointing our important aspects, personality traits, and more, you will be able to select the best realtor for your needs.

1. Patience. Listening Skills and Educative Nature-

first-time homebuyers may have tons of questions. While some of them might be pertinent, others might simply be too trivial. A realtor needs to be sensitive to all the questions, no matter how childish and immature they sound. He or she should be ready to clarify all doubts as well as educate the homebuyers regarding important aspects of the property buying experience.

2. Experience, Expertise, and Awareness about Property Types and Neighbourhoods-

Most realtors specialize in different forms and types of real estate. Some have better awareness about condos and apartments. Others are more into free-standing homes in gated communities. Depending on what kind of property you are going after, selecting a realtor that has prior experience and expertise on the same will help you. The same goes for neighborhoods.

3. Understanding your Racial and Community Needs in Properties-

We spoke about how different neighborhoods in the country have been in the news for racial violence. If you are concerned about the same, it might be a good idea to go with leading Black realtors in Boston. Their understanding of the region can help them inform you about what would be right for you and where you might face problems. This is very important.

4. Having the Right Tie-Ups with Stakeholders-

Leading realtors are a one-stop shop for all your home buying needs and requirements. They can help you with your connections. Whether it be getting loans from banks or fixing the plumbing, they are aware and work with several networks and connections. This can help improve the home buying process and experience. You will have everything done for you.

5. Great Soft Skills and Negotiation Powers-

You want the realtor to negotiate on your behalf in bringing the prices down. If the realtor does not have strong negotiating skills, you might end up paying more than you had imagined. Look at the track and success record of the realtor before going ahead with your decision. A realtor that is good at communication and has a pleasing personality is someone you should aim for.

Where to Find a Realtor that is Perfect for First-Time homebuyers?

If you have been reading the article with interest and focus from the start, your next question would be, where do I find a realtor like that.

In this section, we are going to point out some ways that can help you in your search and discovery-

Firstly, you can start by making recommendations and referrals from your family and friend circle. If someone has recently purchased a new property at a great price, you can request them to hand over the details of their realtor.

Secondly, you can visit online sites that carry detailed information about the realtors in your region. You can go through profiles, connect with them and find out whether they fit the bill of what you are looking for.

Thirdly, you have to check out the online reviews and ratings of the realtors before you hire them. If they have their social media profiles and GMB pages, you will be able to get good information. Make sure to look for how they answer comments.

The Bottom Line

Choosing a great realtor can make all the difference to your first-time home buying experience. Not only do you stand the chance of finding a great property, but they smoothen out most of the problems that you are likely to experience during the process.

If you have any other questions on choosing the right realtors, or on anything related to first-time home buying, let us know in the comments. We will try our level best to clear as many of your doubts as possible.

Read Also:

5 Best Things To Know Before Renting A Property In Kings Cross

What Does it Take to Have an Eye for Top-Notch Properties?

5 Tips to Sell Your House Quickly

In terms of selecting the suitable material for use in industry, two of the most commonly selected products are stainless steel sheets versus carbon steel plates.

The large difference between applications and industries has been widely attached to these due to their durability, versatility, and different performance circumstances.

But both differ significantly in properties and cost-effectiveness; Thus, This will help determine the best-suited material according to specific requirements. So, let's have a closer look at carbon steel vs stainless steel.

Stainless Steel

Stainless steel has carbon, iron, and a minimum of 10.5% of chromium. Chromium is the actual key that reacts with oxygen to form a passive layer to protect the steel from corrosion. This is what reduces the chance of stainless steel rusting.

This is very important if you are looking for outdoor furnishings, or installed something in a wet environment. The higher the content of chromium, the better the resistance to corrosion.

You have to pay attention to the grade of stainless steel when you are buying any appliance and other costly items. Not all materials are created equally.

Stainless steel that a 10.5% chromium is going to cost less than those that have 16% chromium. Moreover, the difference is reflected in service life and maintenance costs.

Main Features of Stainless Steel Sheets

Stainless steel sheets are known for their corrosion resistance that comes with the chemical composition that contains chromium. This makes them be used in most areas where they are usually soaked with moisture, chemicals, and extreme temperatures.

Furthermore, it has an aesthetically pleasing finish, which explains why extensive usage in buildings, kitchen appliances, and medical equipment has been witnessed.

Some advantages of stainless steel sheets include:

Corrosion Resistance: They are even corrosion and oxidation-resistant during these extreme conditions.

Low Upkeep: Stainless steel needs little maintenance, saving time and resources.

Aesthetic Appeal: The outward finish of the finished products is improved through their aesthetic appeal.

Durability: These are very strong and robust, withstanding even high-stress conditions.

To those that produce the highest grade material in the market, these Stainless steel sheet suppliers mainly provide customized products according to a client's needs.

Carbon Steel

Carbon steel is made from iron and 0.12 to 2.00% carbon. The elaborate definition includes alloy steels, which also have 10.5% of alloy content. even though the percentage of carbon is less than two points, it makes a huge difference in the physical appearance and charecteristics like hardness.

When people discuss carbon steel, they refer to the high quality of quality steel used in tools and knives. Carbon steels that have high quality are quite hard, and that is what makes them good at retaining their shape, and resisting abrasion.

They can tolerate significant force before they get deformed. Hard metals are also brittle when extreme tensile strength is applied. High-carbon steels generally crack and do not bend.

Low carbon steel is more easily available than high carbon as they have a low production cost, the ductility is great, and it is also easy to manufacture. Low-carbon steels get deformed under stress but do not break.

Moreover, it is easy to weld and machine the low-carbon steel because of its ductility. They are mostly used in bolts, seamless tubes, automobile body panels, steel plates, and fixtures.

Characteristics of Carbon Steel Plates

Carbon steel plates, In contrast, are priced based on strength and are quite less expensive. This composition is basically made of iron and carbon with just trace elements of practically all other elements. Carbon steel sheets are, therefore, cheaper compared to stainless steel sheets but much less resistant to corrosion.

Some advantages of carbon steel plates include:

High Strength: They can carry heavy loads, making them highly applicable in structural operation.

Cost-Effective: It is relatively cheaper than stainless steel.

Versatility: commonly used in construction work, manufacturing, and heavy machinery.

Elastomer: This may be easily modified through cutting, welding, and other processes.

Generally, Carbon steel plate suppliers serve most industries whenever they require something less costly yet robust.

Carbon Steel vs Stainless Steel: The Difference

Thinking of carbon steel vs stainless steel, but there is no necessary reason to think one is superior to the other. It is all about context.

Every material has its own advantages and disadvantages. The main objective is to match the steel to the requirements. Let’s look at the basic difference at a glance.

Stainless steelHigh carbon steelRust resistantVulnerable to rustLess brittleBrittleLess water-resistantWater-resistant

Applications And Industry Scenarios

Both materials are indispensable in their respective domains. While stainless steel sheets are preferred for applications requiring aesthetics and corrosion resistance, Carbon steel plates dominate in industries demanding strength and economy.

For instance, stainless steel is widely used in pharmaceutical and food processing because of its hygienic quality. On the other hand, carbon steel plates are widely used as a material in shipbuilding pressure vessels and structural frameworks.

About PipingMaterial.ae

PipingMaterial.ae is a prominent online portal where the buyer can contact the best manufacturers and suppliers of industrial-grade material.

This site has thus facilitated sourcing on a business level with verified suppliers of stainless steel sheets and carbon steel plates to ensure quality and reliability.

Whether there's a demand for stainless steel high-performance or even robust carbon steel solutions, PipingMaterial.ae bridges the industrial needs of customers with the genuine stockiest suppliers.

Conclusion

According to particular needs, stainless steel sheets are to be ordered or carbon steel plates are to be ordered. Stainless steel can be a better option than carbon steel regarding corrosion and aesthetic characteristics.

Conversely, carbon steel offers higher strength beyond the competition at an economic cost. With proper advice from trusted vendors on sites such as PipingMaterial.ae, businesses may make proper choices to maximize performance and minimize cost for their projects.

To conclude in the debate of carbon steel vs stainless steel, context is the main focus. You have to decide which one you want depending on the purpose of your need.

Read Also:

Is Steel/Iron Ore A Good Career Path In 2021?

Is Metal Fabrications A Good Career Path In 2023?

Dangers Of Chemical Spills On Humans, Buildings, And Environment

Success on social media requires consistency and engaging in valuable content. Many agents shy away from it due to a lack of time, skills, or content.

Yet, they can still reap the benefits by using automation tools. Platforms like Roomvu offer social media automation services, including content creation and scheduling.

Roomvu’s service does all the heavy lifting, even providing a free content calendar. Agents simply connect their accounts, choose the right content from Roomvu’s content factory, and let the automation handle the rest.

Success on social media requires consistency and engaging in valuable content. Many agents shy away from it due to a lack of time, skills, or content.

Yet, they can still reap the benefits by using automation tools. Platforms like Roomvu offer social media automation services, including content creation and scheduling.

Roomvu’s service does all the heavy lifting, even providing a free content calendar. Agents simply connect their accounts, choose the right content from Roomvu’s content factory, and let the automation handle the rest.