Category: Finance

ContentRally is a leading source of reliable news and trending topics on Finance. Get hard-to-find insights and advice on Finance from industry-specific leaders.

5 Must-Have Long-Term Goals for A Secure Future

Most of us would agree that it’s vital to set goals and make plans to achieve them. People do it all the time. For instance: Goal: ‘Lose 5kg’ Plan: ‘Eat less and exercise more’ But financial goals, which are the life-changing goals of all, are often put on the back burner. Retiring early, setting up a business, or building an investment portfolio worth millions can all seem a bit too hard. You should prepare long-term goals that can help you to achieve your objectives. However, it's not! With a bit of understanding and help, financial goals can be set, plans can be put into place, and the desired nest egg can be achieved. Here are a few long-term goals worth setting: 1. Having an Emergency Fund for The Rainy Days : Life can bring economic uncertainty to many, and even for the financially secure, life happens, in the form of domestic catastrophes, medical bills, and other unplanned expenses. Therefore, it’s vital to have an emergency fund that can offer peace of mind and financial relief in such untoward situations. As a general rule, it’s good to have an emergency fund that would cover three to six months of your living expenses. So, calculate and know how much you need and set aside a certain amount from your paycheck every month. Over the years, this fund will grow, which you can use in case of an unexpected event, or when you are in financial strain. 2. Ditching Debts and Dues for Good : Being in debt can be a stressful experience for anyone, and no matter what your circumstance is, if you have a loan, you are obligated to pay it back. Even if you have life-altering experiences like getting into an accident, losing your job, or increased expenses due to having a child. Hence, repaying the outstanding debt and clearing of all dues is important, especially to know where you stand with respect to money matters. A simple way to clear your debts is to develop a budget that tracks your income and expenses. This will help know whether you have money left over, called the surplus. The goal is to increase the surplus and use it to pay down your debt. 3. Building Your Retirement Fund : Although retirement may feel like a million years away, it doesn’t matter - now is the time to plan for your retirement. Investing and saving is a critical part of leading a financially independent life post-retirement. The good news is, investing even a small amount each month will pay off later in life. Along these lines, decide what you will need during your golden years - expenses like healthcare, household costs, and additional leisure expenses. Once you know your needs, find a suitable retirement plan which can cater to those. Put simply, save, invest, and ensure yourself as a fallback option for your future. 4. Funding Your Child’s Higher Education : Your child’s dreams can become a reality when you support him or her, emotionally and financially. Quality education should be on your and your child’s wish list. Setting up an investment plan that can help with the higher education of your child is a good idea. To do so, find a reliable child education plan that can help you create a substantial corpus for your child’s education and future needs. 5. Expanding Assets for Your Family : Other than making arrangements for expenses, it is essential to create a secure base of wealth for your loved ones so that you can support them and maintain the lifestyle you have now. Investment in unit-linked insurance plans (ULIPs)is a good way to achieve financial growth as well as protect your family’s future in your absence. ULIPs enable you to make significant returns with a relatively low investment every month, while also offering insurance protection to you. Other benefits of unit-linked insurance plans are: Flexibility to choose your fund option- equity, debt or balanced Encourages goal-based saving for child education, retirement etc. The top-up facility gives the flexibility to change your premium amount You can opt for riders like Critical Illness and Accidental Death benefit You get ULIP tax benefits under Section 80C and Section 80D It’s never too late to get started. Pick one or all the financial goals listed above and start setting yourself up for your secure future. Read Also : Getting Your Personal Finances In Order With A Proper Budget Strategy These Small Changes Will Change Your Finances For The Better

READ MOREDetails

Why You Need Classic Car Insurance?

Do you have an old or classic car you would want to insure? When we mean old, we are not talking about 5 or ten years old cars; we are talking about cars made before 1998. If you have such type of car and plan to ensure them to keep their value, there are certain things you need to know. Find out whether your car qualify for classic car insurance Generally, normal car insurance doesn’t have provisions for insuring a classic car. If you need to insure your classic car, may have to take another car insurance policy. For an insurance company like American Insurance to consider you and your car for classic car insurance, there are certain criteria you need to meet. The car must not be your main vehicle. You must have another car you drive more frequently. You should also have a valid driver’s license and secured structure you store your vehicle. Obviously, the car should not be more than 25 years old. If your car is older than 20 years since it was manufactured, you are no longer dealing with a classic car but an antique one. How is the insurance amount determined? Again, your normal car insurance provides coverage up to the actual value of the car. But for classic car insurance, the insurance amount is determined by you and the company. This determination is based on the valuation of the car by research carried out by an underwriter, a professional appraisal, or a classic car valuation guide. What a typical classic car insurance policy covers As stated earlier, a classic car insurance policy differs from the traditional car insurance policy. Apart from providing cover for damage to the car, there are other benefits you can gain from a classic car insurance policy as outlined below. If your personal items are stolen or vandalized, you will be reimbursed If your car is due for the car show but breaks down, the company can offer to pay for your expenses Emergency travel expenses Lost key return Emergency lockout services Roadside assistance Emergency flatbed towing Some companies like American Insurance can cover all of the items listed above while some other classic car insurance companies may provide cover for some. When selecting the best classic car insurance package, it’s important to consider what their policy covers and what it doesn’t cover. That way, you will be able to determine whether the policy is right for you and your car. Difference between normal car insurance and classic car insurance There is obviously a significant difference between your normal insurance policy and a classic car insurance policy. Let’s find out some of those differences. Depreciation or appreciation Your normal car loses value as it gains mileage. But a classic car may appreciate in value, especially when it has been properly maintained. However, your antique car starts depreciating once it has been insured. Based on this reasoning, you are going to receive a lower amount of indemnity if your antique car is totaled (completely damaged) in an accident. Mileage restrictions In classic car insurance, there are certain restrictions placed on the number of times you drive your classic car. However, a normal car insurance policy doesn’t have any mileage restrictions. Lower premiums Classic car insurance premiums of insurance companies like American Insurance are significantly lower than normal car insurance premiums. Sometimes, they may even be lower by 45%, although this depends on other factors as well. Conclusion Owning a classic or antique car is certainly a great investment of your money and time. However, ensuring such a car shouldn’t be much of a hassle for you. There are policies you can take to effectively give protection to your classic car. The above information will be helpful to you when looking for the most ideal option when taking up a classic car insurance policy. Read Also : 7 Reasons Why Teenagers Pay Extra For Car Insurance Tips For Reducing Car Insurance Costs

READ MOREDetails

7 Reasons Why Teenagers Pay Extra For Car Insurance

Car insurance for teenagers is more expensive than experienced drivers. Teenagers, who are at a very young and vulnerable stage of life, often lack any formal driving experience. They learn the skills of driving in this age and polish it with practice. The motor vehicle associations understand the susceptibility of their age and therefore the cost of car insurance for teenagers is higher. In order to understand this concept in detail, we have laid down 7 reasons that “why teenagers pay extra for car insurance”: No Proven Track Record of Driving The insurance companies consider the driving history of the applicant before issuing insurance premiums. In the case of teenagers, there is no proven track record of driving. Since they are at the beginner’s stage of learning, there is no evidence to support their expertise on the road. The risk factor stays high in this case. In general, the people who have proven driving track record without any mention of traffic violations and accidents in their names can avail significant discounts on their car insurance policies. The insurance companies need some statistical proof to make a judgment about the driving skills of applicants- which is not possible in the case of teenagers. Therefore, they cannot assume whether the teenage driver is a safe or reckless driver. In order to cover their risk, they raise the cost of car insurance for teenagers to ensure some safety measures. However, at the age of 19, the insurance plan becomes affordable as you already have 1-2 years driving experience by this time. You can get car insurance here for 19 years olds. Lack of Experience It takes time in learning a skill and achieving expertise in it. Learning to drive certainly takes more time and effort as we face different situations every day on the road. The young drivers need to dedicate a lot of practice hours to polish their skills before they can take their own vehicle independently on the road. The amount of time spent behind the wheel is a considerable factor in enhancing the driving abilities of young drivers. In the case of teenagers, their lack of experience can put them to test while facing real-life driving situations. Their reaction time may be slower than an experienced driver which is much needed when you are in actual driving practice. It is often seen that the young drivers get into a panic very easily when they face unusual situations on the roads. There are research studies to support the fact that most of the accidents that involve youngsters are due to their delay in reaction to the situations that prevail. Emotional Distraction Young people often get stuck with emotional issues. Their vulnerable age often brings out the “rebellious” attitude which may result in anger, sadness, extreme happiness, excitement, overreaction, anxiety, etc. They have very less understanding of dealing with their own emotions which may cause serious troubles while driving. For example- despite many public advertisements, youngsters use their mobile phones while driving. The overconfidence can lead to the accident-prone situation very easily. Youngsters often pool their vehicles and go for diving expeditions. Mutual talking and discussions while driving can distract their attention from the road. It is also common for youngsters to appreciate unusual sights on the road and get diverted from their driving spree. Insurance companies take these facts into account and use substantial proofs to put forth their risk level before issuing car insurance to teenagers. Increased Tendency Towards Speed and Racing There is no denial of the fact that teenagers love formula races and speed games. When they sit behind the steering, they get tempted to race with the cars on their track. Sometimes they have their own bunch of friends racing while driving. The scientific studies have reported that teenagers are easily aggravated by smoking, drugs and alcoholic tendencies. Under the influence of these factors, they may be instigated to adopt risky behaviors while driving. The understanding of the risks and their implications can be attained only with age and experience. The insurance companies state that the lower rates of premiums for the experienced drivers are supported by the statistics that prove that they are less prone to accidents as compared to teenage drivers. The Risk of the Insurance Companies The teenage drivers are at a higher state of financial risks for the insurance companies. The higher the probability of being at risk of accidents raises the probability of higher expenditure of the insurance companies. Therefore, in an attempt to cover the risks associated with the young drivers, they raise the cost of the policy. The Statistical Proofs We have already discussed various factors that may cause teenagers to become riskier while driving. It should be mentioned that our studies are based on statistical findings from various reports. These reports emphasize the high probability of teenage drivers being involved in road accidents. The data has been collected by the years of research that bring the car insurance firms at a higher edge of risk. The Make and Model of the Vehicle We often get to hear that the teenagers are gifted their “favorite vehicle” on their birthday or any other occasions. Although this practice is popular in rich and affluent families, these days even the middle-class segment has roped into the trend. Thanks to the easy loaning facilities! However, parents often forget about the risk associated with allowing teenagers to drive new and expensive cars with high-speed parameters. The insurance companies charge more from their clients who want to purchase insurance of a premium car for their teenager ward. The reason is clearly stated- higher speed parameters of the vehicle are directly proportional to the high financial risk factor of insurance companies. Conclusion Teenagers pay extra for car insurance due to the high amount of risk associated with their age and the levels of maturity. There are facts to support the rash driving incidents leading to fatal accidents in many cases that involve teenagers. Therefore, the higher rates of insurance are just a precautionary measure by the insurance companies. They intend to ensure that the applicant, as well as the company, must be fully prepared to deal with the possible risky outcomes due to driving errors. Higher is the risk of the insurance company, higher is the cost of the premium. Read Also : Tips For Reducing Car Insurance Costs Tips To Lower Your Insurance Costs

READ MOREDetails

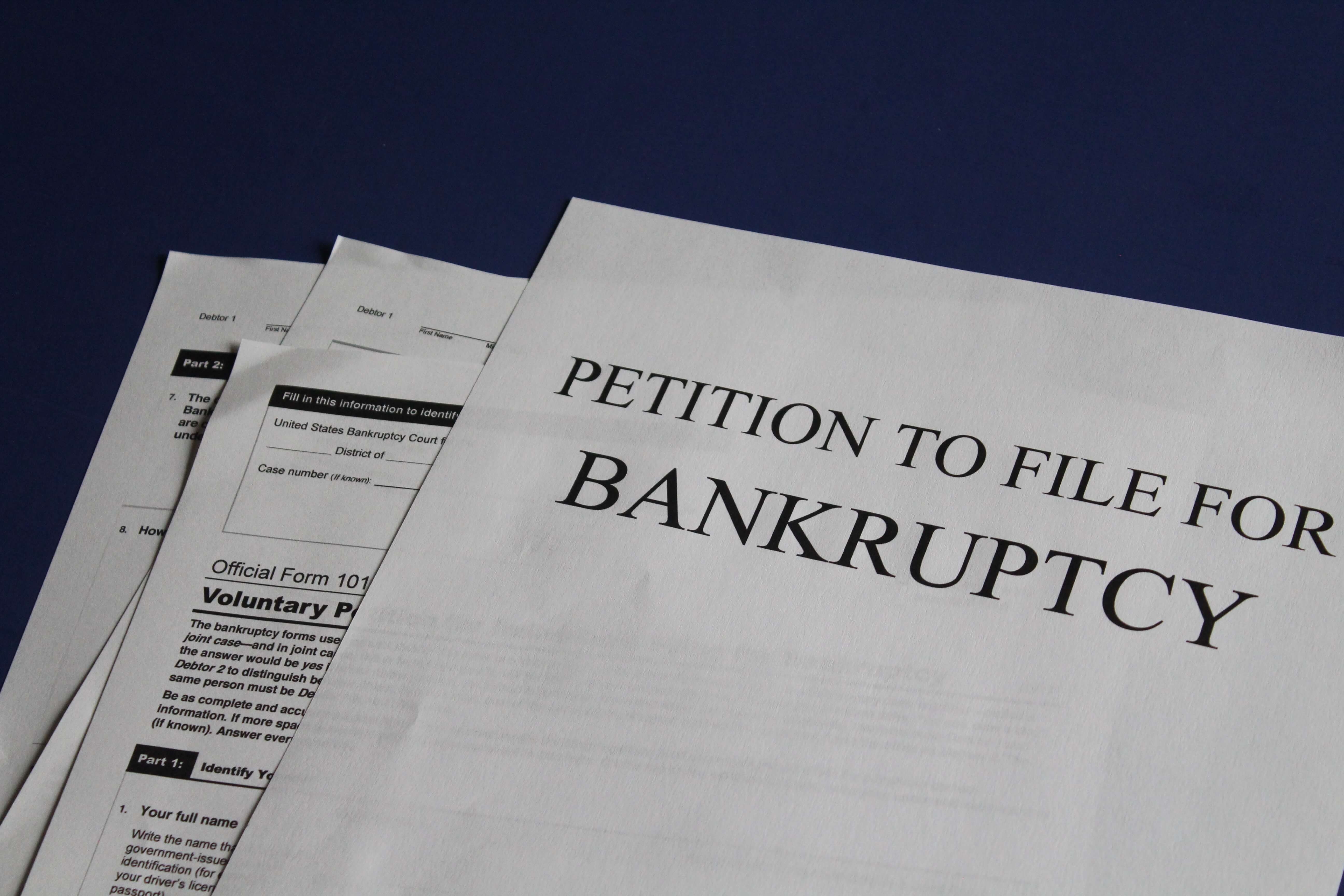

What are the types of debt that can be discharged in bankruptcy?

When it comes to unmanageable debts, it is common to think for a bankruptcy to avoid further issues. The law gives us the opportunity to discharge our debts through bankruptcy in order to recover our financial status. In this article, we are going to talk about the types of debt that can be discharged in bankruptcy. Some of the debts cannot be discharged, but they can be restructured to allow you to pay them easily. Others can be completely eliminated, which will give you the opportunity to keep most of your belongings, rather than selling them to pay off. How does it work? There are two main types of bankruptcy that can be found in Chapter 7 and 13. “Chapter 7 allows you to clean a great variety of debts in a short period of time, while the later Chapter is used to keep your assets in touch.” says Bankruptcy Lawyer Boca Raton With some cases, you’ll have to sell some of your property to pay off creditors. However, if you don’t own much property, you might be qualified as a “no asset” case, which would save you a lot of headaches. Debts that can be forgiven by Chapter 7 include the following: Personal loans Medical Bills Credit card debt Utility bills Repossession deficiency balances Auto accident claims Lease debts Student loans Attorney fees Civil court judgments. With Chapter 13, you can reorganize and consolidate your payments to prevent having any penalties. This way, you can pay most of your debt in a period of three to five years. Upon completion of the repayment plan, you will be discharged by most of the debts that remain. This Chapter is suitable for individuals who wish to keep their assets and those whose income is too high to classify for Chapter 7. To apply for Chapter 13, you must have a solid source of income and enough money left to add them towards your new payment plan. Debts cleaned by Chapter 13: Unsecured Debts Medical Bills Personal Loans Credit card debt utility bills lawsuit judgments income tax obligations The chances are that you’re going to repay some of the amounts through the repayment plan, but the remaining will be discharged. 1. Secured Debts : This chapter allows you to remove debts such as a second mortgage through lien stripping. This way, it will be marked as a non-priority unsecured debt It is important to check all of your debts whether they can be split up. For example, you can split your car loan into two parts - secured & unsecured. Obviously, the secured portion must be paid, while the other one will disappear after the repayment plan is completed. Debts discharged ONLY by chapter 13 Debts accumulated through a property settlement agreement in a divorce Retirement account loans Fines & Penalties owed to the government Condominium Fees Debts from previous bankruptcy that were denied for discharge Debts from malicious damage to a property What Bankruptcy can’t discharge Of course, you can’t discharge all debts using these two Chapters. By using the first one, you will still have to repay the debts after discharge. While using the second, the debts will remain after the repayment plan is completed. Furthermore, if you’d like to keep your personal belongings such as a house or a car, you can’t omit payments Non-dischargeable debts: Debts accumulated due to a personal injury caused by driving under the influence. Student loans Fines and penalties for violating laws Child & Family support Income tax debts within the past three years. If your creditor is against your request to discharge the following debts, they might be classified as non-dischargeable. Debts from willingly causing an injury to a person or property Debts owed due to a divorce settlement Debts due to fraudulent activity Credit purchases for luxury goods within the last two months. Bankruptcy will surely not solve your financial problems, but it will ease your situation, allowing you to make timely payments and recover quickly. Read Also : Debunking 7 Notorious Bankruptcy Myths Major Financial Problems That Can Affect A New Business What Are The Benefits Associated With Crowdfunding For Businesses?

READ MOREDetails

HybridBlock: Why Binance Is Investing In Crypto-Fiat Trading

Binance is currently known as one of the largest cryptocurrency exchange firms in the world. Changpeng Zhao heads the company, and he recently unveiled that the company will be focusing on a shift to trade cryptocurrencies for fiat money. According to Zhao, this move would make it possible for investors to perform an increased number in trading volume, an increased number of participants in the market, higher liquidity, and more speculators. He said that it would also boost the trading industry, and more people will be drawn to the world of cryptocurrency which will bring positive effects to the industry. Changpeng Zhao’s idea was lauded by financial experts around the world, saying that his plans for the future of cryptocurrency exchange are one of the most plausible given the factors that affect the market today. Zhao has been a veteran in the financial industry, and he previously established several companies; one of them is Fusion Systems which was founded in 2005 and presently headquartered in Shanghai. It became his stepping stone to know more about trading and how the financial world works. As cryptocurrency started to develop and to draw in more investors, Zhao decided to learn more about this new mechanism in the financial industry. He chose to join Blockchain.info in 2013 to develop his skills in dealing with cryptocurrencies, and he successfully learned new tips and tricks on how to become successful by trading cryptocurrencies. He, later on, founded several other companies that relied on blockchain technology, and in 2017, he decided to establish Binance. Initially establishing the company’s headquarters in China, Changpeng Zhao decided to move it in Japan after the government started pressuring him. He later opened offices in Taiwan, while at the same time looking at how his company grew tremendously. In 2018, Zhao expressed his idea of moving his company to Malta after he received several warning letters from the government of Japan and Taiwan. They are telling him that his company is not registered, and there can be legal consequences if he did not abide by the country’s financial rules and regulations. Despite these warnings, Binance continues to grow, and in 2018, it managed to gain a market capitalization worth more than $1.3 billion. It is more successful than traditional banks, and Zhao stated that the future is bright for their company as he sees that cryptocurrency will further increase in value. Changpeng Zhao stated that after his company completed its transfer to Malta, he will enable their users to convert the digital tokens that they have in their wallets into various fiat currencies. He also added that Malta is one of the few countries on Earth that are supportive of cryptocurrency traders, just like him. He wanted to transfer his operations in Malta because he said that there would be fewer legal problems in the small European island state. The government of Malta is working hard to persuade cryptocurrency giants to transfer their operations to the tiny Mediterranean Island. Malta wants to become known as the Blockchain Island, and they are developing new legislation that would encourage cryptocurrency traders to transfer their operations. One of the most important advantages of the idea proposed by Zhao would be the generation of new cryptocurrency traders and the balance to the world economy that it would bring. If the participants in the market increased, it would signal a rise in the demand for more cryptocurrencies, and it would transform the whole industry into one that could easily surpass traditional companies that are not keeping up with technology. Zhao wants to change how the world looks at the global economy, and he stated that his idea could become a reality. According to Zhao, fiat money is one of the best materials to be traded for cryptocurrency because it has a designated value given by the government. He is optimistic about the effects of his decision on the future of trading, and he believes that more people will become aware of its advantages. He continues to inspire a lot of people because of his perseverance to create new mechanisms that would innovate the financial sector. The experts who are working with the largest financial companies are saying that Binance have really shaken up the competition in the industry, and they are hoping for more people like Changpeng Zhao to come out and increase the competition in the sector. Read more about Changpeng Zhao and Binance at the HybridBlock Blog. Read Also : Hiring A Blockchain Developer 5 Awesome Facts About CryptoCurrency What Should Be There In An ICO Whitepaper? Expert Take

READ MOREDetails

How to become a sub-broker?

To become a reputed and successful entrepreneur, it takes hard work. In India, the opportunities for launching new businesses are umpteen, but the competition is fierce. There is no magic mantra that can help one company find success within record time. It requires dedication, perseverance, and knowledge. Sub-brokers are entrepreneurs with immense potential for making a profit. They are not trading members of stock exchanges, but they can act on the behalf of one. They can also assist business owners and new investors to buy or sell securities through registered trade members. The opportunities of a sub-broker business are plenty. If you have a fair idea of the share market and its products, it is going to be a rewarding business for you. In fact, it is a rewarding profession for novices as well. Anyone with the aptitude for share trading and the will to learn about the share market should be able to master the necessary skills of a sub-broker. What are the necessary qualifications of a sub-broker? The qualifying criteria remain more or less constant across the country for sub-brokers. Here’s a list of the edibility requirement for joining the elites – The person should have a graduate degree. Any subject should do, but the aptitude for share trading is a must. The applicant should have passed their 10+2 examinations at the least. They should know about the financial markets of the country. They should either have the qualification that gives them the knowledge of it or previous experience that gives them the insight of the share markets. He or she should also be able to manage basic financial transactions. They should have the latest information on the economic, socioeconomic, political and environmental scenario in the country. That is because every change in the scenario impacts the share market. They should know how to operate computers. The applicant must also be able to learn specific trading and monitoring software necessary for the process. Nothing can replace good communication skill for sub-brokers. They should be able to convince and comfort their clients during and after investment. It is a highly competitive niche and reliable skills of communication can give you an edge over your competitors. They should be good at management. You must remember that every business is about great management. Nothing can take the place of management when it boils down to man, market, and money. The aspiring sub-broker should clear the basic NISM modules on mutual funds, equities, F&O, and commodities. These regulations ensure that all sub-broking work should follow the completion of these modules. How to find a stockbroker to work with? Next, it is time for the sub-broker to find a broker as a partner. It is the most crucial step towards setting up the sub-broking business and you need to keep a few things in mind before you go down this path – i. Pick a good broker Finding a good stockbroker does not mean looking for one with a lucrative office or higher profit share. The broker you should look for should be reputed in the market, should be trustworthy and active. Make a list of the priority values you want to see in your stockbroker. Consult with your friends, family and fellow sub-brokers during the selection process. Check the broker’s profile before you go into business with him or her. ii. You should be ready for the full-time commitment Being a sub-broker is not a part-time hobby. It is a business and a full-time commitment. You will almost never be off the clock. Even when you will be away from your desk, you will be receiving updates on your mobile phones. Staying connected 24/7/365 will ensure that you will always be ready when a big business opportunity knocks on your door. iii. You need to be more than the average sub-broker Clients expect a lot more than the usual assistance and dealing. It is a competitive market, and you need to cater to your clients’ needs for market advice, investment aide, and product selection. Every client now deals in multiple products like mutual funds, currency, equities, and securities. It has become the responsibility of the sub-broker to advise them on the selection of products to avail the best investment opportunity at the time. What are the finishing touches of becoming a fine sub-broker? Get your own client database Becoming a good sub-broker takes a lot of practice and time. It is important to have databases of people, who are likely to become your clients soon. It is possibly the only profession where cold calls are still valuable and useful. The first stage of the database may consist of your family, friends, ex-colleagues and social media contacts only, but you need to start working on that data. You will have to go through multiple rounds of meetings with your clients, explain the prospects, your business USP and their chances of making profits in the long run. Build your network Finding a reliable sub-broker is a challenge for many regular share market clients. You need to fill that gap and become the sub-broker they can trust. So, do not push sales from the first round of calling and meeting. Ask for references once you establish a relationship with the client. Attend networking meetings. They might be a tad bit cliché, but they are always effective in getting new leads for the new sub-broker. Yes, you should expect to find them the moment you step in. It will take some time for others to warm up to you and for you to notice the new opportunities in the market. Keep yourself updated Lastly, no great sub-broker can remain great without regular brush-up of their market knowledge. So, go ahead, install some of the best market update applications, follow rewarding share trading blogs and follow the news on the changes in the financial policies of the country that can affect the market. To offer your clients a little more than the next sub-broker is offering, stay updated with the international market news as well. The ups and downs of the global market always influence the prices in the Indian share market. Read Also : How To Choose The Best Broker For You How Real Estate Factors Into Business Decisions

READ MOREDetails

Introduction to StockEdge – Overview and important Feature

1. Daily Updates : Who doesn’t like to get all the updates about financial markets at one place in a short and crisp manner? Stock Edge provides this feature in the “Daily updates” section. You just have to dedicate 5-10 minutes of your day to this section and you are ready with all the updates for the day. It also helps those people who do not have much time to spare and still want to keep a track of the day-to-day activities of the markets. 2. Scans : Scans make it very easy for the user to filter out stocks that he wants on the different basis. For example, if the user wants to filter out stocks on the basis of profitability, he/she can use the fundamental scans, and if he/she wants to filter out stocks on the basis of technical scans like simple moving average scans, Relative Strength Index scans (RSI) etc., and he/she can do so by using the technical scans. Likewise, there are many other scans available in the StockEdge application like price scans, volume and delivery scans, futures scans and options scans etc. The user can select the scan that he/she finds suitable and make scans accordingly. For more detailed knowledge about each of the section of the StockEdge application, click here 3. Learn Section : There is even a “Learn Section” on the StockEdge homepage. In this section, many useful materials for your reference are available as shown in the image below. These materials are free to use by anyone who is using the StockEdge application. This section is a combination of different content that has been developed to know the concepts of financial markets. What does it include? It includes basic and advanced levels of capital market and financial market. It includes both written material and videos by an expert. 4. Tracking FII/DII activity : Who are FIIs/DIIs? Foreign institutional investors (FIIs) refers to people from other countries who are investing in Indian companies and Direct Institutional Investors (DIIs) are Indian Institutional Investors who invest in Indian Companies like banks, financial institutions, insurance companies, mutual funds etc. What do they signify? These traders trade in huge quantities so they have the capability to influence the movement of the market. This data helps in tracking the inflow and outflow of the money in the Indian market. With the help of this data, one can track in which segment of the market, these investors are investing their money in whether cash market, futures market, stock options or stock futures. 5. Tracking what big investors are doing : This section gives you a list of all the investors that purchase shares of a company for long-term because they believe that the company has strong growth prospects in the future. Tracking these big investors helps in getting an idea of where should one invest their money in only after proper study and “doing your homework”. Suppose, you want to track the big bull of India, i.e. Rakesh Jhunjhunwala, all you need to do is type his name in the search box and you will get a list of people or institutions that are in any way related to Rakesh Jhunjhunwala. You can add all of them in your “investor group” and keep a track of them just by clicking on the group. 6. Search by Sector : One can even search a stock by sector wise. For example, if you want to study how the automobile sector is performing, he/she can just click on the “sector” section and go to the automobile part. All the stocks are classified on the basis of the different sector which makes it easy for anyone to study a particular sector. Bottom Line : Stock Edge is best for anyone who does not have much time to invest in the stock market and still wants to earn returns higher than the bank deposit. StockEdge helps you to be your own analyst by providing with all the data that you need to analyze a company. How to download the StockEdge application? For Android (Google Play Store) users, you can click here to download the app. For iOS users, you can click here to download the app. You can also check out the video below for a better understanding of the application. Link:-https://www.youtube.com/watch?v=h8ooI9Fo7Dg Stock Edge provides you with all the analysis you required for self-research. However, if you still feel that you need a more customized learning environment, we present StockEdge club for you. This is India's first virtual club for stock market enthusiasts. This club will have the following features - Access to 12 paid webinars that we conduct on a monthly basis. Invitation to become part of one workshop in your city or in the nearby city. Become a part of a What's App group where there will be continuous learning, continuous doubt clearing, and continuous question and answer so that you become a more knowledgeable and learned participant of the financial market in India. To know more about this, you can click here. Read Also : Best SEO Tools For Ranking The Website How To Check Someone Out Online: 5 Tips On Finding Out Someone’s Personal History How To Remove Pname Com Facebook Orca 10 Of The Best Facebook Pages To Follow Now

READ MOREDetails

A Beginners Guide to Investing: Getting Started in 8 Simple Steps

Did you know that 61 percent of people find investing scary or intimidating? This number is even higher when it comes to millennials. Investing in the stock market isn't just something super clever people do. You don't have to be really wealthy to start investing in stocks. But you do need to know what you're doing before you get started. That's why we've put together this beginner's guide to investing. Get started with our guide to investing in 8 simple steps. 1. What is Investing? Instead of just putting your money into your bank account and allowing it to earn interest, an investment is a risk. You're not guaranteed any returns on your investment. Therefore, you have the chance of making a lot of money if you play your cards right. But you also could make a mistake resulting in less money than with which you started. You can even lose it all. There are multiple different kinds of investments you can make. These include: Shares Funds Bonds Property (check out Turner Investment Corporation for a place to start) Whiskey Land Antiques This includes everything from the conventional shares and funds to the less obvious whiskey and antiques. It's basically anything that you believe will increase in value over time. But for our purposes, it's best to focus on the stock market. This involves buying shares in one or more companies to make a profit over time. When most people think of stock markets they imagine lots of young and flashy stock brokers shouting "buy!" and "sell!". But the truth is that it's much more boring than this. It's actually about selecting a number of shares or funds, tracking how they're doing and pulling out when you think it's a good time. 2. Stock Markets and How They Work A stock market is just a place where people come together to buy and sell shares in companies. Each share is listed on what's called an exchange. But how do shares come about? Companies provide investors the chance to support what they're doing with cash. This allows the company the chance to grow and the investor to make money on the back of this success. When you invest in a company, you become a shareholder. You can trade this share in the company with anyone else who wishes to purchase it from you. Even though the original price of each share is determined by the company itself. From thereon, the price of each share is influenced by a number of factors from the strength of the overall economy to the financial health of the company. Depending on these factors, the price of the company will rise and fall in the stock market. 3. How Much Can I Make by Investing? This is the real reason why people start investing in stocks. They want to make money. But there's no simple answer to the question of how much you can make. But it's worth pointing out that in the current economic climate, savings rates are actually at an all-time low. This means that many people are searching for alternative means of making money. How much you can make by investing is also contingent on how bigger risk you can afford to take. The more you're willing to risk, the higher the potential of your returns. 4. How Much to Invest? So many people spend many years of their lives thinking that when they finally have some spare cash, they'll invest it. But this is actually the wrong way to look at investments. You don't need piles of cash to start investing. By investing a little amount regularly, you can build up your returns over time. It's important not to invest everything you've got in a single venture. "Not to put too many eggs in one basket" is excellent advice for any wanna-be investor. Together with traditional ways of investing, you should also look to put some money in alternative investments. You have to be able to afford to lose the money you're thinking of investing. If there's a stock market crash you could lose everything you've invested overnight. You should also make sure you can afford to put money into a share over a minimum of 5 years. You need to be able to plow through the bumps along the way to make anything in the long run. 5. What's a Share? Let's investigate a little further what a share actually is. It's a unit of value of a company. If a company is valued at $10 million and there are 1000 shares, each share would be worth $10,000. But the shares of the company can rise or fall according to the overall value of the company. People invest in a company because they believe the company will be successful in the future. By buying shares you get the chance to share in the success or failure of the company. Along with the profit you make when the shares increase in value, as a shareholder, you usually receive dividends too. This is a payment to you by the company from the profit generated by the company. 6. What's a Fund? If you want to buy shares, you can either purchase stocks or funds. Instead of purchasing the shares from the company, you pass your money to a fund manager. The fund managers bring together the money of a number of investors and purchase shares on the stock market for you. 7. How to Start Investing? There are a number of different ways to purchase shares and funds. But most people use what's known as a platform to make purchases. You have to select which platform you want to use to make your investments. After you've done this, you can select which investments you want to make. Confused? Think of it as buying milk from the store. You have to choose which store (your platform) you want to purchase the milk. And then you need to choose which milk (your investment). You'll also be charged for your shopping bag (user fees). 8. Should I Invest? Of course, it's always good to evaluate why you're investing in a particular company. Ask yourself - is investing right for you? History shows us that people who invest in shares over savings accounts receive greater returns. But this doesn't necessarily mean that investing is for everyone. Guide to Investing: Investing can often seem confusing and scary to the uninitiated. But the truth is it's much simpler than it appears. By following our start guide to investing, you can start making informed decisions about what you want to do with your spare cash. For more blog posts on financial issues, check out our blog. Read Also: Investing In Machinery For A More Productive Business What You Must Know About ELSS Before You Invest

READ MOREDetails

Major financial problems that can affect a new business

For a new business just fresh out of the concept stage, there’s a lot of excitement ahead. However, there are often troubles on the horizon, and these tend to revolve around money issues. Finance streams may be in place when the business is first created, for example, but they can quickly dry up as time goes on. It’s expensive to hire staff, and this can often push a firm well into the problem zone. Here are some ways that new businesses can get around these problems. No finance streams : When a new business first launches, it’s usually the case that there’s some form of finance behind it – at least for a short time. The entrepreneur themselves might be financing it from savings, for example, while there may also be an investor. The long-term plan is usually to have incoming cash replace this stream once it dries out – but revenues and profits don’t come overnight, and in fact, they often don’t materialize for a long time. Instead of relying on external finance providers, it often makes sense for a new business to be “bootstrapped”. Bootstrapping essentially means cutting down costs until you reach a stage where you have the funds to raise them back up. Instead of hiring an office space, for example, why not knuckle down and work hard in your spare room until you have enough – or almost enough – sustainable income to pay for a desk somewhere? It may be tough doing this sort of thing at first, but it could be the difference between business survival and failure. Staffing costs : In a bygone age of manufacturing and industry, the main cost that businesses faced was equipment. This also tended to be where companies made cutbacks when times were hard, either by downsizing their factories, leasing out their equipment or something similar. However, for many modern American businesses, the main cost is staff. Staff members are, in general, expensive. Some, such as coders and executives, command high salaries that can quickly drain a firm’s budget. Even when a person is hired on a lower salary, there are plenty of extra considerations to take into account, which can make the hire expensive: from the additional insurance premium that a firm might need to pay on their office space to the additional computer and desk space that the staff member might need, the costs can mount up. It makes sense for many firms to hire contractors instead of as they come with far fewer financial responsibilities for the firm – and the arrangement gives both parties the flexibility to move on if needed. With umbrella companies available to manage the tax side of contractor pay, there’s no need to worry about the effect that it might have on your HR or accounting departments either. Running a new business is exhilarating in some ways, but it also comes with its problems. Finance is almost always the big one – and from large staffing costs to dried-up finance streams, there’s a lot that can go wrong. However, by focusing on finance methods such as bootstrapping and choosing contractors instead of employed workers, there are ways that you can get that profit and loss sheet under control and move towards a more sustainable financial future for your business. Read Also : Invest In A New Car, Without A Financial Liability Debunking 7 Notorious Bankruptcy Myths

READ MOREDetails

7 TIPS TO REDUCE CREDIT CARD BILLS

If you have a large amount of credit card debt and you are only making minimum payments every month, you are not going to pay it off any time soon. In fact, if you only make minimum payments, it could be decades before you find yourself debt-free again. It is extremely important to put yourself in a proper financial position, and a good way of doing that is by reducing your credit card bills. Tips to reduce Credit Card Bills: Here are a few tips on how to reduce your credit card bills that will help you pay off your debt: 1. Take Stock: Before you start to reduce your credit card bills make sure you know where you stand. By this, we mean know your target. You will never hit the target if you don’t know where it is, so be honest with yourself. 2. Pay more than the minimum: As discussed before, if you only make minimum payments each month, then it will take ages before you find yourself debt-free again. Thus, it is clear that paying more than the minimum due you can lower your monthly credit card bills, but still, so many customers struggle in making that the priority. Making a little more than the minimum payment every month will eventually help you in the long run. 3. Ask your credit card company for lower rates: A simple and quick way to lower your credit card bill is by negotiating a lower interest rate. Just by reducing the rate of interest by one or two percent, you can save hundreds of bucks. Try calling your creditors and ask them politely to lower your rates. If you have a good credit score and have been a loyal customer to them, then you can easily negotiate and get yourself a lower interest rate. 4. Target one card at a time: People often use multiple credit cards to buy stuff. More cards mean more accounts which eventually leads to more debts. If you are using multiple credit cards, then a good way to lower the bill is by targeting one card at a time. Focus on one account and try to clear that first. Get the minimum for each card, but pay as much as you can on the card you are targeting first. Usually, paying the card with the highest interest rate works. 5. Make a budget: Make yourself a budget every month and stick to it. It can be difficult to adjust your lifestyle too quick, so instead, try going for small adjustments. It can be as simple as cutting out one or two pizzas each week or by changing your thermostat by few degrees. Reducing your costs a little bit can help you out in the long run. Remember to save yourself a few extra bucks every month in case an unexpected bill pops up. 6. Make two minimum payments every month: A good way to lower your bill is by making two minimum payments. Since credit cards apply interest daily, cutting your balance during the month will reduce the minimum payment for the next month. 7. Transfer your balance: Another good way to reduce your monthly payments is by transferring the balance from a card with a high-interest rate to a card with a low-interest rate. If done properly, this can save you hundreds of bucks every year. Remember that credit cards with a low rate of interest are mostly introductory offers which last about a year and a half, so make sure pay off the debt before the rate of interest increases. Conclusion: We hope these tips can help you to reduce your credit card bills. If you know more tips on lowering the bill, post them in the comment sections below! hence if you want to make your choices in the right direction then the use if the credit card bills can make things work for you in all possible manners. Work out the best strategy that can help you to achieve your objectives in the best possible ways. Read Also : Are Debt Consolidation Loans Recommended For Credit Card Consolidation Credit Card Fraud The Holiday Season: Things To Consider For Next Year What Are The Important Parts Of A Free Business Credit Report?

READ MOREDetails

Hiring a Blockchain Developer

You can hire a Blockchain developer if you have a startup online company that is dealing with Bitcoins, financial services, insurance, asset management, banking, healthcare, supply chain management, music and entertainment, and personal identification services, etc. The digital form of transactions can be made secure, simple, and with the design and development of customized applications for your specific requirements. Hire Blockchain Developers - Specifications and Benefits You can get most of the Blockchain developments done through open-source programming languages. For example, you can think of Python, Java, PHP, C++ and related languages, which are mainly used in the programming languages paradigm. They are cost-effective compared to licensed programs. Moreover, they have continuous updates and upgrades in technology that are easily accessible online. With minimal investments, you can get maximum benefits from programming done within a short span of time. Security: Blockchain developers ensure maximum security for your coding information. It is primarily due to the multiple levels of encryption using customized algorithms. No hacker in the world will be able to break open the coding system accurately. The developers can create perfectly anti-hacking systems that can detect hackers and block them from basic levels. So, it is technically impossible to decode. Moreover, the native coding techniques of C++ and Java make it more complicated to hack. The other aspect is a complex structure of database structure. In most of the cases, programmers use indexing, hashing, and cryptographic systems to store data. Since they are also encrypted multiple times, it is impossible for any hacker to take out the data in its entirety and use it for breaking into online transactions. Combination of encryption and decryption techniques between transaction input and output will be known only to the developer and his team. So, you can feel secure about financial and Bitcoin transactions online. Efficiency: Native coding is more efficient and faster compared to heavy coding from licensed software applications. They take up highly limited space on a disk storage system. At the same time, they perform faster. Their efficiency of data gathering, processing, and transaction execution is much higher than the other legacy high-end languages. When you hire a Blockchain developer, he will ensure maximum output generation with minimalist coding techniques. Abstraction: Abstraction is one of the key elements that influence the efficiency of programming. By following the abstraction and polymorphism methods of OOPS, the Blockchain developer can create closes bonding between the objects and data. It will not be possible to access them since they are made abstract. Moreover, the location of the actual code that drives Blockchain technology will keep changing on the network. Developers can store them in your local computer behind firewalls. Only the copies of those programs will be working online. It is easy in such a programming environment to make changes to the original coding without affecting the running programs in any way. The developer can update the programs according to your specific requirements and update them onto the server when the users have logged off the system. When the user's login next time, they find the newest version of the system. Queries: Apart from writing main programs for transactions, the Blockchain developer can generate user interface programs that answer their queries. They can handle thousands of user queries within seconds and provide satisfactory answers for all of them. Customer satisfaction levels will always be the highest when you hire a Blockchain developer. He can interlink the backend queries with any kind of user interface front end. For example, you can consider the HTML, DHTML, and advanced graphical UI for mobile and smartphone apps. Blockchain developers can link the backend with an existing app, or develop new apps that are specific for Android, IOS, Windows mobile, tablets, PCS, Mac and Linux systems. This approach makes the program development platform-independent in the real sense. Customer Satisfaction: Consider a typical case in which one of your customers wants to know about his Bitcoin transaction status and history from a remote corner of your state. His request will be interpreted by the Blockchain program that is resident in a remote server. Data may be located in yet another remote location of secure servers. When you hire a Blockchain developer, he will be able to integrate all these components together in one piece of code and user interface. Your customer will be able to get the required results and reports within a fraction of seconds. So, you can expect him to refer your business brand to thousands of his contact circles. It is the best way of online marketing you can ever expect to happen for your online business. Increasing customer satisfaction can get you consistent business growth. Predict Markets : Prediction of cryptocurrency values in the online markets is getting increasingly speculative. You will never know when the value reaches the peak and when it may hit the lowest value. When you hire a Blockchain developer, it is possible to get the best hints about changing trends in advance. It is due to the algorithms and coding techniques used by the developer. Trough his programs, he will be able to predict future trends based on facts. He can gather these facts from the leading global and local markets consistently and in real-time. So, he can generate secure user interface screens through which you can monitor cryptocurrency markets very closely. Legalize Trade : Cryptocurrency trading and transactions could be made perfectly legal and secure from government police when you hire a Blockchain developer. Through him, you will develop principles and practices of programming that are transparent for the law enforcement authorities. Now, you can run your online businesses by getting License. It is one way of ensuring maximum customer trust. They will be ready to invest in your business since they are sure of getting returns without any legal and taxation hassles. So, you can soon convert your startup company into an online enterprise within the shortest span of time. Your business can become a globally recognized brand name. Read Also : 5 Awesome Facts About CryptoCurrency What Should Be There In An ICO Whitepaper? Expert Take How To Choose Best Virtual Private Network In Poland

READ MOREDetails

Debunking 7 Notorious Bankruptcy Myths

Bankruptcy is a serious step in anyone’s life and can have serious consequences. However, in many cases, bankruptcy is the only way out for some and can bring about the much-needed change as it helps them get rid of old debts. Understanding how bankruptcy affects you is key when deciding whether to file for bankruptcy with the help of experienced attorneys such as the BK Lawyers. People often turn to familiar people who have been through the same thing or try to find answers regarding bankruptcy on the internet. And while in some cases this might provide the answers they seek, in others, it may bring a lot of misinformation. There’s no reason to turn to unreliable sources for advice when in most cases bankruptcy attorneys don’t charge the initial consultation during which they can provide answers to all the questions you may have about the process. Therefore, we recommend consulting an experienced attorney before consulting the internet. To help you better understand bankruptcy, we are going to debunk some of the most common myths. You Can’t Travel Overseas after Filing : Many people believe filing for bankruptcy prevents you from traveling overseas. However, the truth is that a trustee will let you travel overseas as long as you make the required payments and provide the required information. You’ll also need to provide financial information regarding the trip, for example, who’s financing it, where you’re traveling, etc. Filing for Bankruptcy Costs a Lot : As we mentioned, the initial bankruptcy consultation is usually free. Reliable sources you can consult about bankruptcy include trustees, insolvency experts, and AFSA. You’ll Love Everything : One of the most common myths is that filing for bankruptcy means you’ll lose all your assets in order to pay off your debt. Depending on the debt, you may be allowed to keep a lot of assets including your household items, furniture, and appliances. You may keep a significant portion of your balance to cover the costs of living. In some cases, you may be allowed to keep your vehicles to a certain value, as well as tools of the trade. However, most people worry about losing their home. And even if your home has to be sold to cover your debts, you may arrange to purchase it from the bankruptcy trustee. Your Earning Will be Limited : There are no limits to your earning when you file for bankruptcy. However, if you earn more than a certain level you’ll need to make some contributions every year during the period of bankruptcy. The Debts you leave off the Bankruptcy Form are Not Included : When filing for bankruptcy you need to submit a form listing all your assets and debts. This form is called a Statement of Affairs form. Leaving information out of this form is considered an offense for which you may be criminally prosecuted. While you need to fill out the form as precisely as possible, leaving out a debt unintentionally will not affect whether that debt will be included in the bankruptcy. You Have to File for Bankruptcy if You Can’t Pay Your Debts : There are other ways to cover your debts, but in most cases, bankruptcy is the most effective one. Bankruptcy has a minimal impact on your finances if you’re not able to cover your debts through selling assets and earnings. IF you have a higher income or have reasons to avoid bankruptcy (if you’re a CEO) you can refinance your home, arrange a debt agreement or make informal arrangements to cover the debt. You’ll Never Get a Loan Again : While your bankruptcy is recorded in the credit report seven years after filing and it’s recorded in the NPII, there are still ways to help people with bankruptcy get back on their feet. Credit providers are willing to assist individuals who filed for bankruptcy to get a loan despite that.

READ MOREDetailsPopular

Technologies For Creating A Startup Idea

20 Feb 2023

How to Download Facebook Videos on Android?

07 Feb 2019

7 Rules of Effective Ecommerce Web Design

28 Jan 2021