While there are many people who started their business in the year of the pandemic as a result of the outbreak of the Coronavirus in 2020, many people found it challenging to make their minds about which type of business to start.

While some people started their small businesses at home with the MVP development, there were many who began opening their cafes and restaurants. There are also people who completely shifted their line of work and started their pharmaceutical sector.

For those who used the pandemic as a turning point to build long-term financial security or diversify assets, exploring international business hubs became a smart move. Hong Kong, with its strong legal system and financial infrastructure, is a top destination for entrepreneurs who want to create a trust fund — whether to protect family wealth, plan for succession, or support global investment goals.

In this article, I will be guiding you through the concept of a business model called scalable startup entrepreneurship. So in case you want to know more about this type of business, keep reading this article till the end…

Scalable Startup Entrepreneurship: What Is That?

Now at first, you might get confused when you hear the term scalable startup entrepreneurship. But calm down a bit. And think what it literally means.

Do you need some help? Here I am.

There are many types of startups in the world. Some of the most important types are small businesses, buyable, lifestyle, and scalable. In this article, I will be focussing on scalable startup entrepreneurship.

Scalable startup entrepreneurship is a business model where business owners or new entrepreneurs start their business on a relatively new idea. It aims at making a lot of profit after achieving very high growth.

The main focus of such businesses is to improve the profit by delivering satisfactory services to the clients or customers and turn them into their lead. The essential factor that drives the company towards making a very high profit is its working strategy and the structure of the business.

Read More: Self-Improvement Tips For Managers

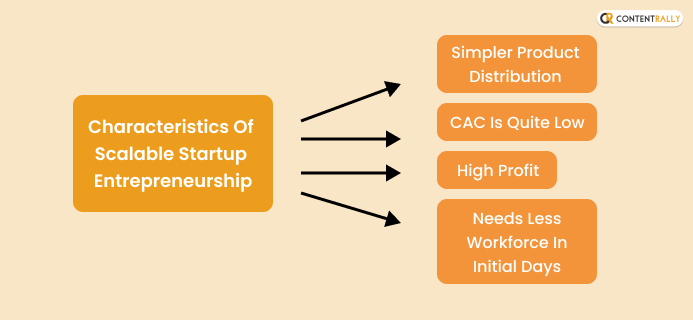

Characteristics Of Scalable Startup Entrepreneurship: How To Know What It Is?

The most important thing that needs to be present to start scalable startup entrepreneurship or business is the characteristic of scalability. They start their brand or business with the vision and goal in mind that they can make a difference.

Other essential characteristics of the scalable startup entrepreneurship are:

1. Simpler Product Distribution

One of the significant characteristics of scalable startup entrepreneurship is the fact that it has a very inexpensive cost of delivering the product to its target audience. By that, I mean that the method of product distribution is quite simple and, thus, cheaper.

2. CAC Is Quite Low

The Customer Acquisition Cost or CAC of the startup is lower than other companies. This is because scalable startups do not need to spend a lot of money to grow their business. Instead, they do that simply with the help of the organic growth of the startup. This, in turn, reduces the CAC of the startup.

3. Needs Less Workforce In Initial Days

Scalable startup entrepreneurship is a business idea that starts small and goes on to get higher profits. This means that in its initial days, the company or startup begins with a very minimal workforce or people to operate the company.

Click Here To Read: How To Make Your Online Business More Humble By Managing Your Reputation

4. High Profit

One of the most essential characteristics that make up the various scalable startup entrepreneurship is their high-profit margin. This is because they are able to control the prices of the commodities and run their business to maintain a profit that is relatively high.

Strategies To Follow For Your Scalable Startup Entrepreneurship

In case you were confused about how to go about your scalable startup business, I have the best deal for you. Keep reading below for some of the strategies that can help you to grow your business.

Here are some of the most straightforward strategies for your scalable startup:

1. Create A Business Plan

One of the most important things that you need to keep in mind while beginning your scalable startup business is that you must have a solid business plan.

A business plan is needed as it helps you to ensure that you know what to do next. In addition, it allows you to stay focused by giving you and your startup the direction that it needs.

2. Make Technology Your Friend

One thing that you must remember is that you need to make the use of the right tech. This can help you deliver satisfactory results to your customer and help you retain them.

When you are able to retain your target audience and turn them into your sales lead, they will ensure that you are able to grow your company.

You May Like To Read This: Small Business Entrepreneurship – Small Business, Strategies And Many More!

3. Get The Help Of Social Media

Social media is an excellent place if you want to look for some exposure. It helps you to reach your target audience within a very short span. The reach that you achieve with the help of social media platforms is effective and can help you to grow your business.

Scalable Startup Entrepreneurship Examples: Know Who To Follow!

Scalable startups are a business model that starts small and depends on the benefits of technologies to grow fast and big. Some of the most important examples of these scalable businesses are as follows:

- McDonald’s

- Amazon

- AliExpress

Frequently Asked Questions (FAQs):

There are many scalable startups that have come into existence in the past few years. Some examples of scalable startups are Instagram, Facebook, and Twitter.

A scalable or scalability business is one in which the company improves its profit as they grow. Their business idea is unique, and they work on their work strategies to reach their goals.

The scalable startups are the ones that have unique ideas when they start. They also have a solid strategy to begin their work and run their business successfully. The main aim of these businesses is to ensure that they earn high income through their working strategy.

Wrapping It Up!

Scalable startup entrepreneurship or businesses are those businesses that start with a unique idea. But, at the same time, they aim to earn a high profit through their marketing and work strategies.

Many types of scalable startup entrepreneurship exist today in this world. Some examples of this type of entrepreneurship that are scalable are Facebook, McDonald’s, and Instagram.

In case you were looking for the meaning of scalable startup entrepreneurship, I hope that you have found this article to be of help. In case there are any other queries regarding the same, feel free to write them down in the comment section below.

Let me know what you think about this article. And if you believe that you can start scalable startup entrepreneurship, go for it!

Till then, stay safe and dream big!

Read Also:

- How To Become An Entrepreneur?

- A Checklist Of Tools For A Successful Advertising Agency

- Social Entrepreneurship – Entrepreneurship Strategies And Many More!